By Invitation

Insights into the Gold & Bullion market

Over the past two years, gold prices have been underpinned by strong physical demand from China and central banks. However, investor flow, and specifically retail-focused ETF building, resident- its easing cycle on September 18, the Fed projected 50 basis points of rate reduction by year's end and a full percentage point of decreases the following year.

During times of global instability and low interest rates, gold is typically favoured as an

investment. The U.S. presidential election on November 5th may possibly lead to a further

increase in gold prices, as investors may seek safe-haven assets due to possible volatility in

the markets.

Global Factors Impacting the Gold Rally

Gold has been the best-performing asset class in 2024, rising around 30% in international

markets and 22% in domestic markets with prices surpassing the $2700/oz (~ Rs 76400)

mark. The global central banks’ ongoing gold purchases, the US Federal Reserve’s rate cuts,

the geopolitical unpredictability of the world’s markets, the slowdown in the Chinese

economy, and the recent monetary stimulus measures taken by the Chinese central banks

are all responsible for the strong performance.

1) Central Bank Buying

This year’s central bank gold demand is probably being influenced by the gold price

increase, but the long-term pattern of net purchasing is still in place. Total gold holdings

added by central banks around the world from January to July is around 520 tonnes. Turkey,

India and Poland have been the top buyers, while the Philippines and Thailand are the net

sellers.

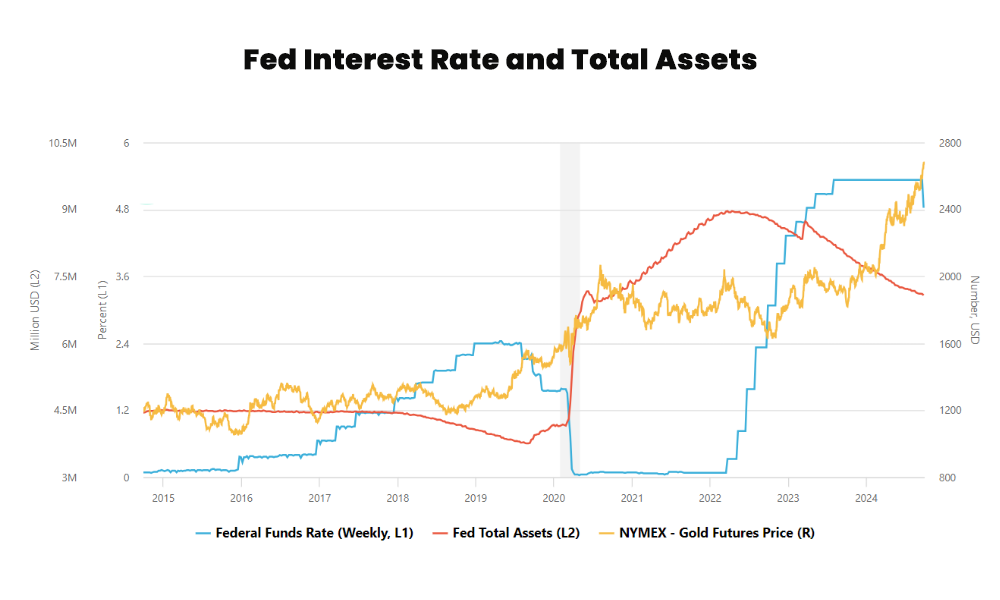

2) FED rate cut cycle

Even if inflation is still high, gold is still in a favourable position as the Federal Reserve

cuts interest rates to support a contracting labour market. After a 50-bps rate cut and a

warning that rates may drop to 3% by 2026. It’s evident that the Fed is relaxing, which is

good news for yellow metal. With central banks all over the globe starting to lower

interest rates, gold is still the primary hedge against currency devaluation on a

worldwide scale.

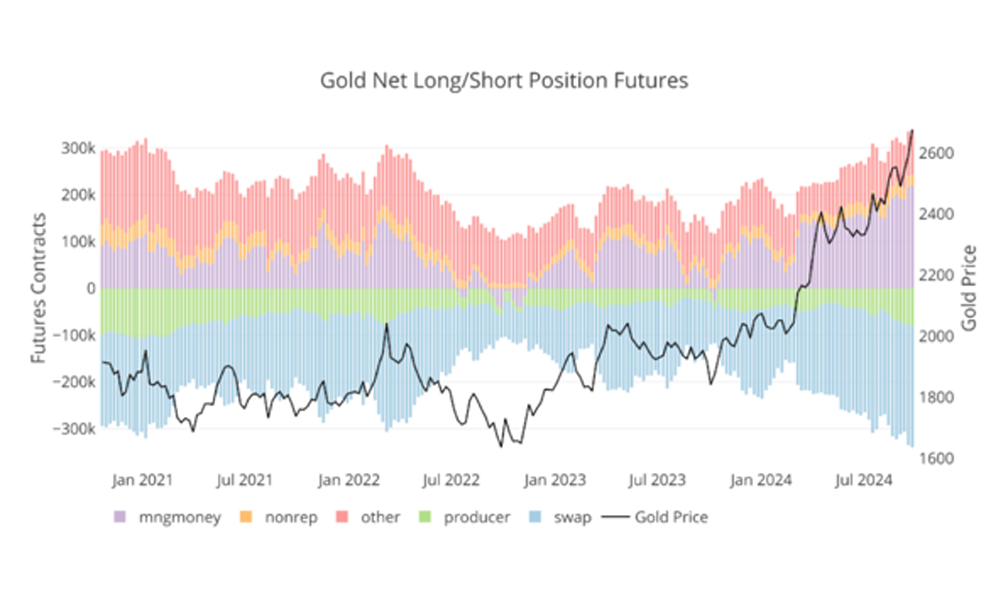

3) Gold CFTC positioning

Due to the ongoing rate-cut cycle by the Federal Reserve, geopolitical worries in the Middle

East, and expectations of increased festival demand in India, investors are still building long

positions in gold. U.S. traders have lately entered the speculative phase headed by China,

with futures long holdings at a nearly four-year high (315,000 contracts), producing a

market that is mostly unaffected by normal drivers.

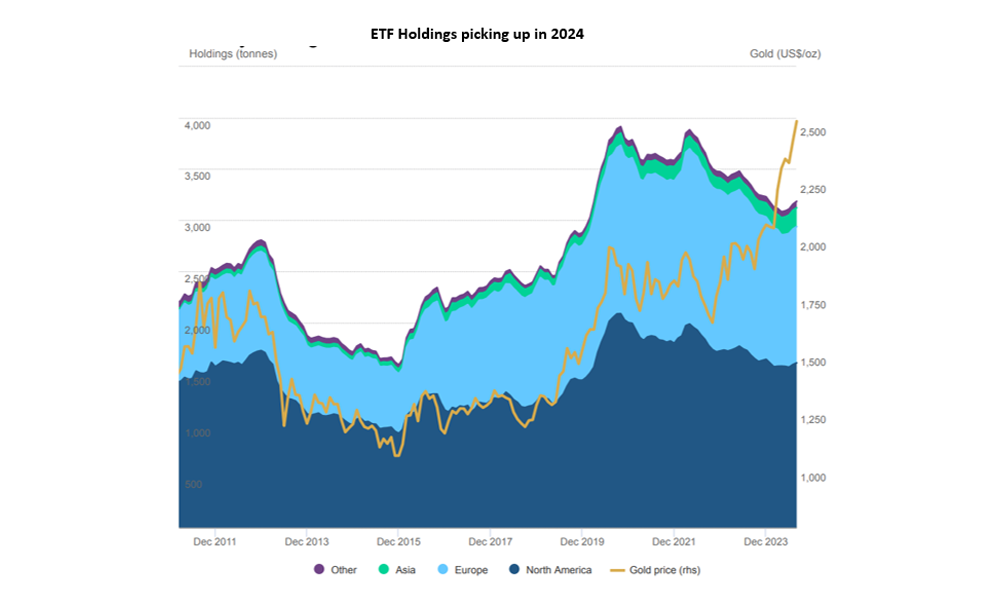

4) ETF Holdings

Four months in a row, there have been inflows into global gold ETFs: all regions had positive

flows, with Western funds leading the way. The y-t-d losses for global gold ETFs further

decreased to $1bn as a result of nonstop inflows between May and August. Additionally, the

2024 holdings reduction has been reduced to 44t. In the meantime, during the first eight

months of 2024, the total AUM increased by 20%. Asia has seen the most inflows this year

($3.5 billion), while the leading outflows are from North America (-$1.5 billion) and Europe

(-$3.4 billion)

5) Dollar index

The Dollar Index has slipped below the highly crucial psychological milestone of the 100

mark as the US Dollar’s role as the major global reserve currency is being threatened. The

combination of better risk sentiment and lowered Fed rate expectations is fundamentally

unfavourable. Since gold doesn’t generate interest, cuts in interest rates contribute to a

declining value of the US dollar, which in turn makes the non-yielding metal more appealing.

The dollar index’s negative relationship with gold keeps the yellow metal maintained at high

levels.

6) Gold Silver ratio

The gold-silver ratio dropped to its lowest levels since July during the last week of

September, when gold started to approach $2700 and silver momentarily overtook a 10-

year high of over $33. At this point, the gold-to-silver ratio is 84 to 1. The beginning of a

silver rally that would see white metal surpass its more costly counterpart would be

confirmed by a sustained decline in the gold-silver ratio.

Domestic Factors Supporting Gold

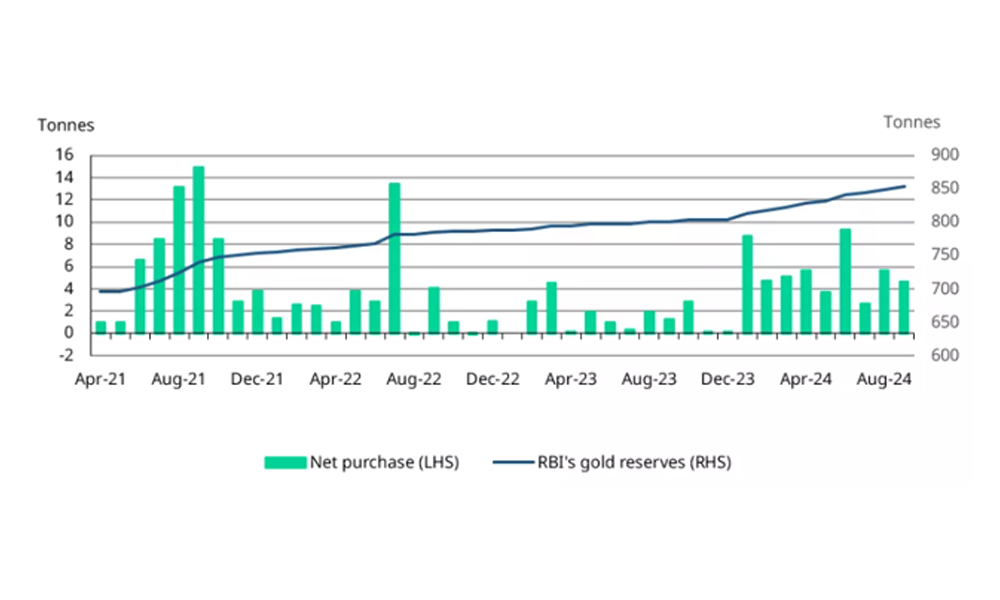

1) RBI Gold reserves

The Reserve Bank of India’s appetite for gold remains high, as indicated by its recent

acquisitions. Over the first eight months of the year, the RBI has acquired a total of 50

tonnes of gold, with acquisitions in each month. Up from 7.5% a year ago, the RBI’s gold

reserves have now reached a record 853.6 tonnes or 9% of its total foreign reserves.

2) India Gold Imports

The Union Budget’s announcement of the reduction in import duties and the modifications

to the long-term capital gains for gold ETFs has contributed to the rise in gold imports into

India. Between January and August, gold imports increased by 30% year over year to almost

485 tons, valued at US$32 billion.

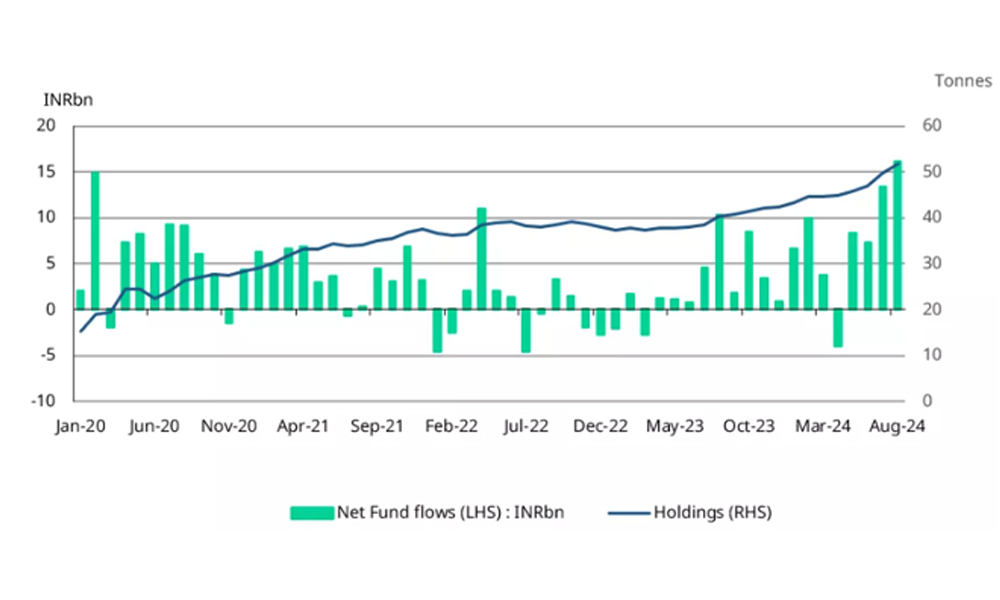

3) Gold ETF Holdings

Investor interest in Indian gold ETF has surged since the end of July. According to AMFI data,

net inflows into Indian gold ETFs have reached Rs 61 billion (~$735 million) thus far in 2024,

a considerable rise of over Rs 15 billion during the same period in the previous year.

Together, these funds have added 9.5tn of gold this year, increasing their total holdings to

51.8tn, a 29% year-over-year rise.

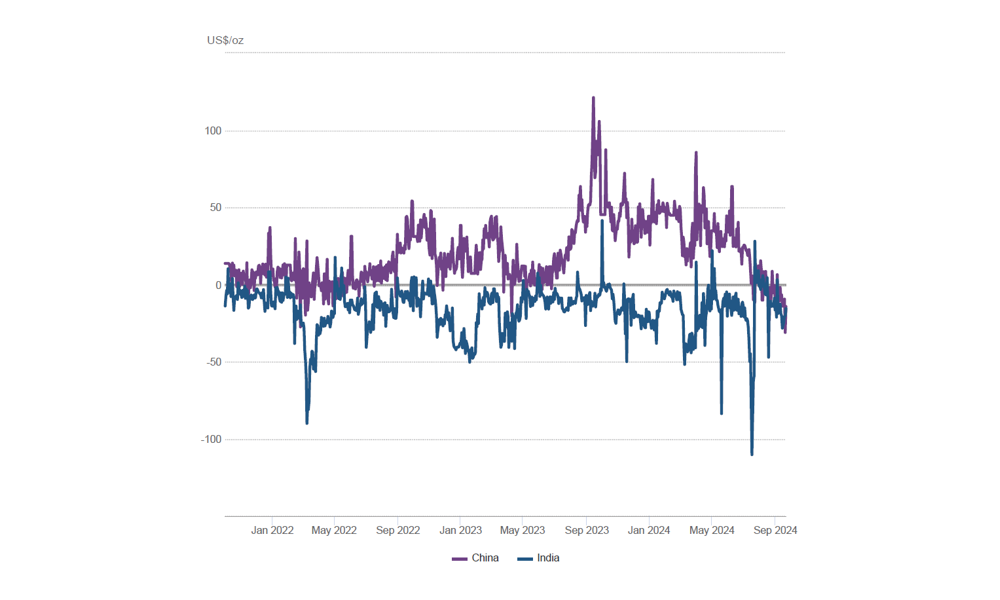

4) Gold Premium/Discount

The gap between domestic and international gold prices has narrowed as a result of rising

global prices and increased supply from increased imports. Domestic gold prices have been

trading either at a modest discount to or in line with international prices in recent weeks,

despite the normalizing but still robust demand.

Diwali Outlook

Overall, with continued global economic uncertainty, gold is expected to retain its appeal

as a hedge against inflation and market volatility. Investors may adopt a “buy on dips”

strategy as the metal is likely to see periodic fluctuations, but the long-term outlook

remains bullish through for next 5-6 months and prices are expected to touch $3000 (~Rs

84000).

Having said that, currently gold prices are in the overbought zone, so we might see a

consolidation phase and a retracement with support at $2575 (~Rs 73000) and resistance

being the next psychological level of $2750 (~Rs 78000) in the next one month.

By Invitation

From Prompt To Pendant: How AI Is Turning Jewellery Buyers Into Designers

By Dr Sandip P. Dhurat

Not long ago, jewellery design was largely a one-way conversation. Consumers browsed catalogues, visited stores, or selected pieces from showcases. If they wanted something custom-made, they relied on the jeweller’s sketches, imagination, and expertise.

Today, a new collaborator has entered the room: Artificial Intelligence.

Across age groups, consumers are experimenting with AI-powered image generators and design applications to create jewellery concepts that reflect their personal tastes. A few words typed into a prompt—”an emerald engagement ring inspired by lotus petals” or “a contemporary mangalsutra with geometric motifs”—can generate multiple design possibilities within seconds.

What happens next is perhaps the most interesting part of the story.Instead of ordering these pieces online, many consumers are taking their AI-generated designs to the one person they trust most: their family jeweller.

The new wave of customisation

For decades, customization in jewellery was often limited to engraving names, changing gemstones, or making minor design alterations. AI is expanding that possibility dramatically.

Consumers are no longer arriving at jewellery stores with vague ideas. They are walking in with detailed visual references generated on their smartphones. Some have experimented with dozens of versions before settling on a favourite. Others blend elements from different designs to create something entirely unique.

In a sense, AI is democratizing the design process. It allows consumers to participate creatively, even if they have no formal design background.

For younger buyers especially, this level of involvement is appealing. They want jewellery that feels personal, expressive, and different from what everyone else is wearing. AI gives them a playground where they can explore possibilities before making a purchase.

Role of traditional family jeweller

If AI can generate designs so easily, does that diminish the role of the jeweller?Quite the opposite.

While AI can create attractive images, it cannot determine whether a design is structurally sound, comfortable to wear, practical to manufacture, or durable enough for daily use. A ring that looks spectacular on a screen may be impossible to cast. A delicate bracelet generated by AI may not withstand regular wear.

This is where the expertise of the jeweller becomes invaluable.

Family jewellers are increasingly acting as interpreters between digital imagination and physical reality. They assess AI-generated concepts, refine proportions, suggest technical modifications, and ensure that the final piece balances aesthetics with craftsmanship.

Many jewellers describe the process as similar to working with a client-provided sketch—except the sketch is now more sophisticated and visually detailed.

The trust factor remains unchanged. Consumers may discover designs through AI, but they still want someone they know to guide the process and stand behind the finished product.

New collaboration trend

The relationship between customer and jeweller is evolving from buyer-and-seller to co-creators.

Consider a young couple designing an engagement ring. Instead of selecting from existing collections, they use AI to explore various combinations of settings, gemstones, and motifs. They then sit down with their jeweller to discuss feasibility, budget, stone availability, and craftsmanship.

The final piece is neither entirely AI-designed nor solely jeweller-designed. It is the outcome of a collaborative journey.

This shift creates opportunities for jewellers to engage customers more deeply. Conversations become richer because customers arrive with visual ideas rather than abstract descriptions.

In many cases, the design process becomes part of the emotional value of the jewellery itself.

The opportunity

The trend presents several advantages for jewellers willing to embrace it.

First, AI-generated concepts can serve as conversation starters. Instead of spending significant time understanding a customer’s vision from scratch, jewellers can begin with a visual reference and refine it together.

Second, it can increase demand for bespoke jewellery. Consumers who might never have considered custom design are discovering how accessible it has become.

Third, it opens the door to a new generation of buyers who value individuality over mass-produced designs.

Rather than competing with AI, jewellers can position themselves as the experts who transform digital concepts into heirloom-worthy creations.

Despite all the excitement around AI, jewellery remains an intensely human product.

A necklace gifted on a wedding day, a ring marking an engagement, or a bracelet passed down through generations carries emotions that no algorithm can replicate. AI may help generate ideas, but it cannot understand family traditions, cultural significance, sentimental stories, or the subtle nuances of personal taste.

Consumers are discovering designs through technology, but they are still seeking reassurance, expertise, and craftsmanship from people they trust.

Perhaps that is the real story behind this trend.

AI is not replacing the jeweller. It is empowering consumers to participate in the creative process while making the jeweller’s role even more valuable. The screen may provide the inspiration, but it is the skilled hand of the jeweller that transforms a digital concept into a treasured piece of jewellery.

In the years ahead, the most successful jewellers may not be those who resist AI, but those who embrace it as another tool in the ongoing art of personalization—where technology sparks the idea, and craftsmanship gives it life.

Jewellery-Inspired Eyewear Emerges As Fashion’s Latest Luxury Statement

BlueStone, SafeGold Launch Platform To Convert Idle Gold Into Digital Assets

De Beers Narrowed Losses In H1 2026 Despite A Sharp Decline In Rough Diamond Prices

Kalyan Jewellers Unveils Akshaya Thanga Maligai (ATM) As Its First Regional Brand; Sivakarthikeyan Named Brand Ambassador

De Beers Narrowed Losses In H1 2026 Despite A Sharp Decline In Rough Diamond Prices

Jewellery-Inspired Eyewear Emerges As Fashion’s Latest Luxury Statement

-

BrandBuzz1 day ago

BrandBuzz1 day agoKalyan Jewellers Unveils Akshaya Thanga Maligai (ATM) As Its First Regional Brand; Sivakarthikeyan Named Brand Ambassador

-

International News8 hours ago

International News8 hours agoDe Beers Narrowed Losses In H1 2026 Despite A Sharp Decline In Rough Diamond Prices

-

National News8 hours ago

National News8 hours agoBlueStone, SafeGold Launch Platform To Convert Idle Gold Into Digital Assets

-

JB Insights7 hours ago

JB Insights7 hours agoJewellery-Inspired Eyewear Emerges As Fashion’s Latest Luxury Statement