By Invitation

Insights into the Gold & Bullion market

Over the past two years, gold prices have been underpinned by strong physical demand from China and central banks. However, investor flow, and specifically retail-focused ETF building, resident- its easing cycle on September 18, the Fed projected 50 basis points of rate reduction by year's end and a full percentage point of decreases the following year.

During times of global instability and low interest rates, gold is typically favoured as an

investment. The U.S. presidential election on November 5th may possibly lead to a further

increase in gold prices, as investors may seek safe-haven assets due to possible volatility in

the markets.

Global Factors Impacting the Gold Rally

Gold has been the best-performing asset class in 2024, rising around 30% in international

markets and 22% in domestic markets with prices surpassing the $2700/oz (~ Rs 76400)

mark. The global central banks’ ongoing gold purchases, the US Federal Reserve’s rate cuts,

the geopolitical unpredictability of the world’s markets, the slowdown in the Chinese

economy, and the recent monetary stimulus measures taken by the Chinese central banks

are all responsible for the strong performance.

1) Central Bank Buying

This year’s central bank gold demand is probably being influenced by the gold price

increase, but the long-term pattern of net purchasing is still in place. Total gold holdings

added by central banks around the world from January to July is around 520 tonnes. Turkey,

India and Poland have been the top buyers, while the Philippines and Thailand are the net

sellers.

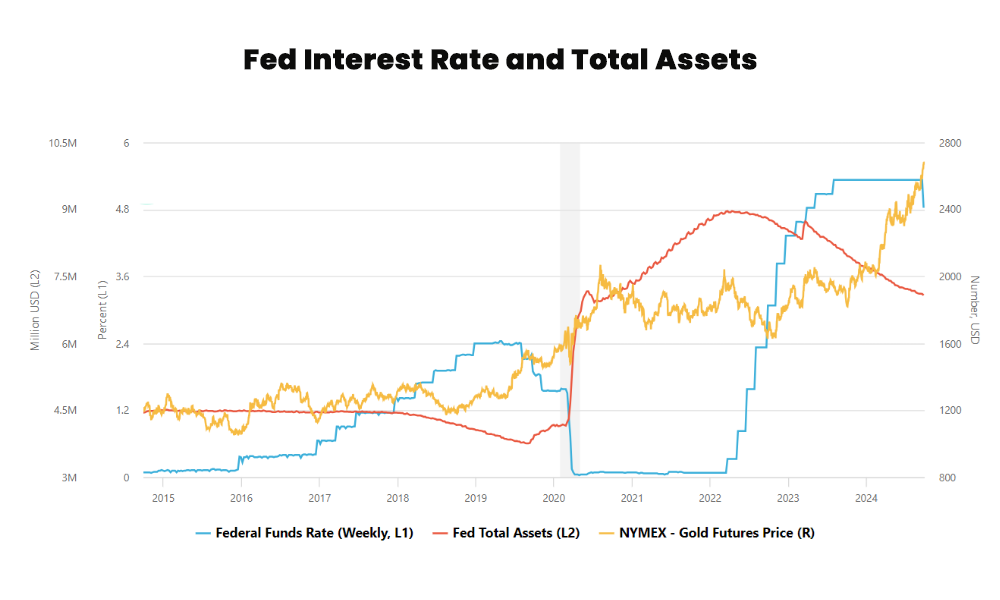

2) FED rate cut cycle

Even if inflation is still high, gold is still in a favourable position as the Federal Reserve

cuts interest rates to support a contracting labour market. After a 50-bps rate cut and a

warning that rates may drop to 3% by 2026. It’s evident that the Fed is relaxing, which is

good news for yellow metal. With central banks all over the globe starting to lower

interest rates, gold is still the primary hedge against currency devaluation on a

worldwide scale.

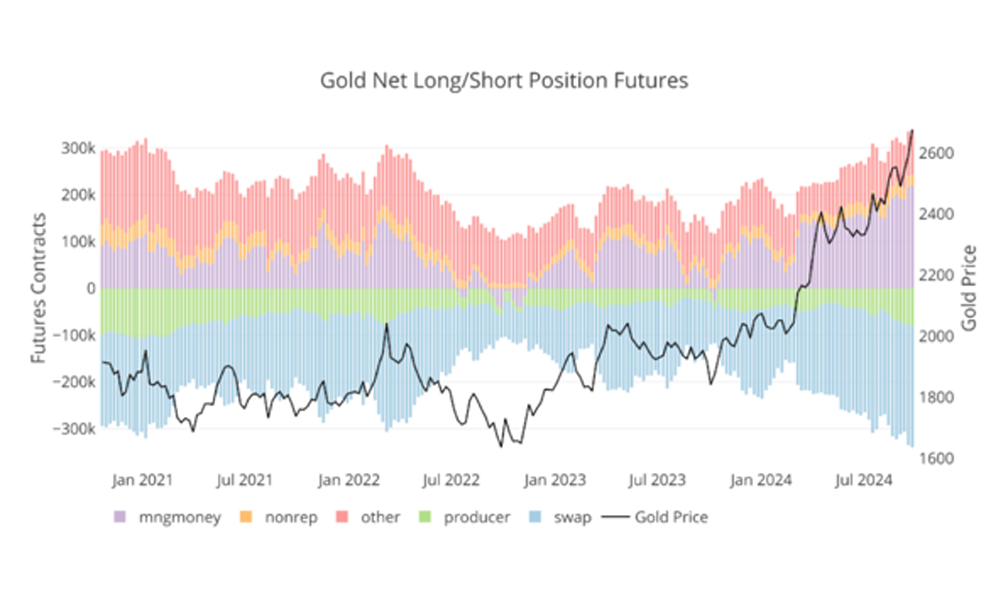

3) Gold CFTC positioning

Due to the ongoing rate-cut cycle by the Federal Reserve, geopolitical worries in the Middle

East, and expectations of increased festival demand in India, investors are still building long

positions in gold. U.S. traders have lately entered the speculative phase headed by China,

with futures long holdings at a nearly four-year high (315,000 contracts), producing a

market that is mostly unaffected by normal drivers.

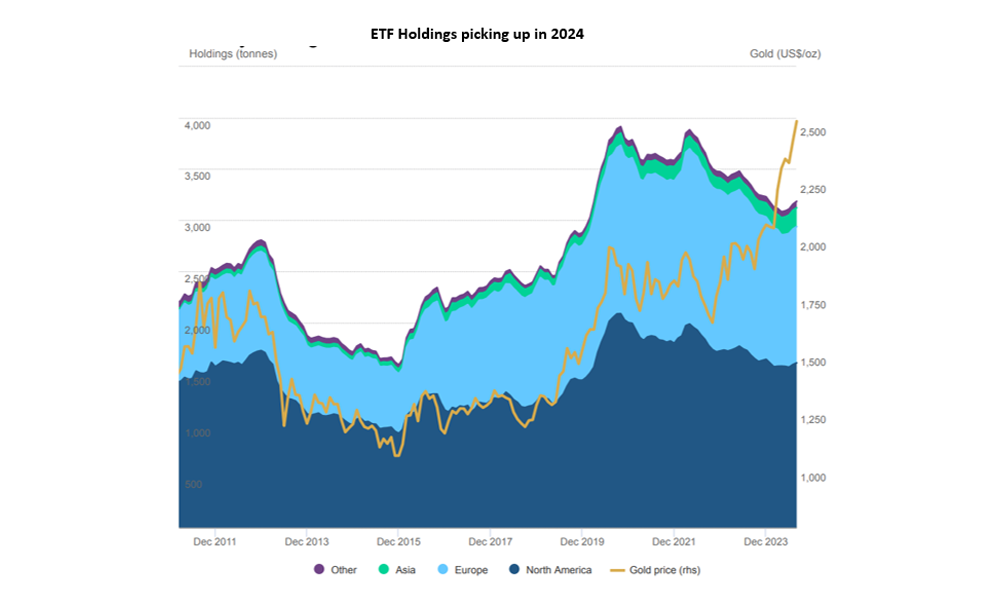

4) ETF Holdings

Four months in a row, there have been inflows into global gold ETFs: all regions had positive

flows, with Western funds leading the way. The y-t-d losses for global gold ETFs further

decreased to $1bn as a result of nonstop inflows between May and August. Additionally, the

2024 holdings reduction has been reduced to 44t. In the meantime, during the first eight

months of 2024, the total AUM increased by 20%. Asia has seen the most inflows this year

($3.5 billion), while the leading outflows are from North America (-$1.5 billion) and Europe

(-$3.4 billion)

5) Dollar index

The Dollar Index has slipped below the highly crucial psychological milestone of the 100

mark as the US Dollar’s role as the major global reserve currency is being threatened. The

combination of better risk sentiment and lowered Fed rate expectations is fundamentally

unfavourable. Since gold doesn’t generate interest, cuts in interest rates contribute to a

declining value of the US dollar, which in turn makes the non-yielding metal more appealing.

The dollar index’s negative relationship with gold keeps the yellow metal maintained at high

levels.

6) Gold Silver ratio

The gold-silver ratio dropped to its lowest levels since July during the last week of

September, when gold started to approach $2700 and silver momentarily overtook a 10-

year high of over $33. At this point, the gold-to-silver ratio is 84 to 1. The beginning of a

silver rally that would see white metal surpass its more costly counterpart would be

confirmed by a sustained decline in the gold-silver ratio.

Domestic Factors Supporting Gold

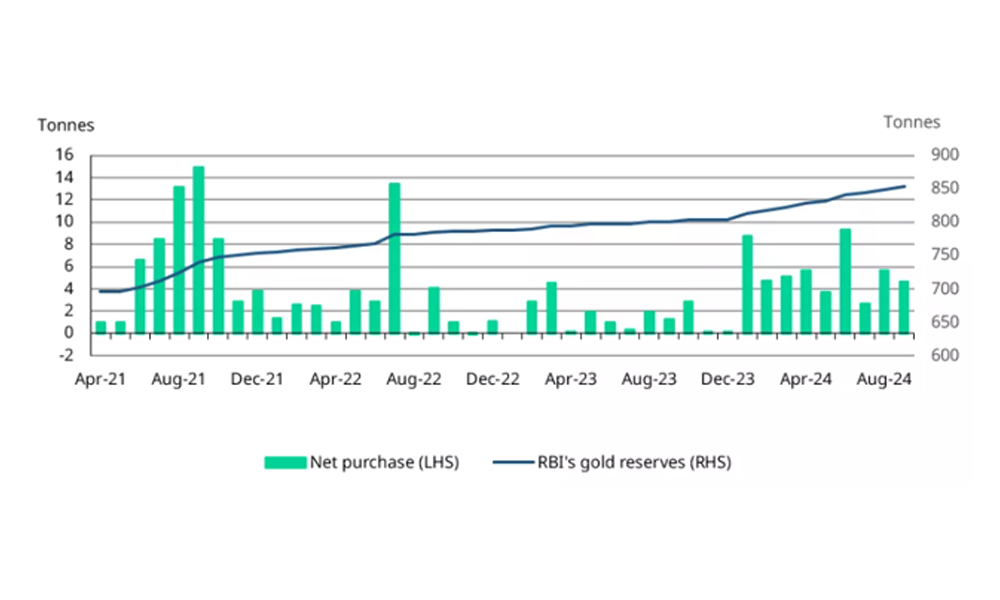

1) RBI Gold reserves

The Reserve Bank of India’s appetite for gold remains high, as indicated by its recent

acquisitions. Over the first eight months of the year, the RBI has acquired a total of 50

tonnes of gold, with acquisitions in each month. Up from 7.5% a year ago, the RBI’s gold

reserves have now reached a record 853.6 tonnes or 9% of its total foreign reserves.

2) India Gold Imports

The Union Budget’s announcement of the reduction in import duties and the modifications

to the long-term capital gains for gold ETFs has contributed to the rise in gold imports into

India. Between January and August, gold imports increased by 30% year over year to almost

485 tons, valued at US$32 billion.

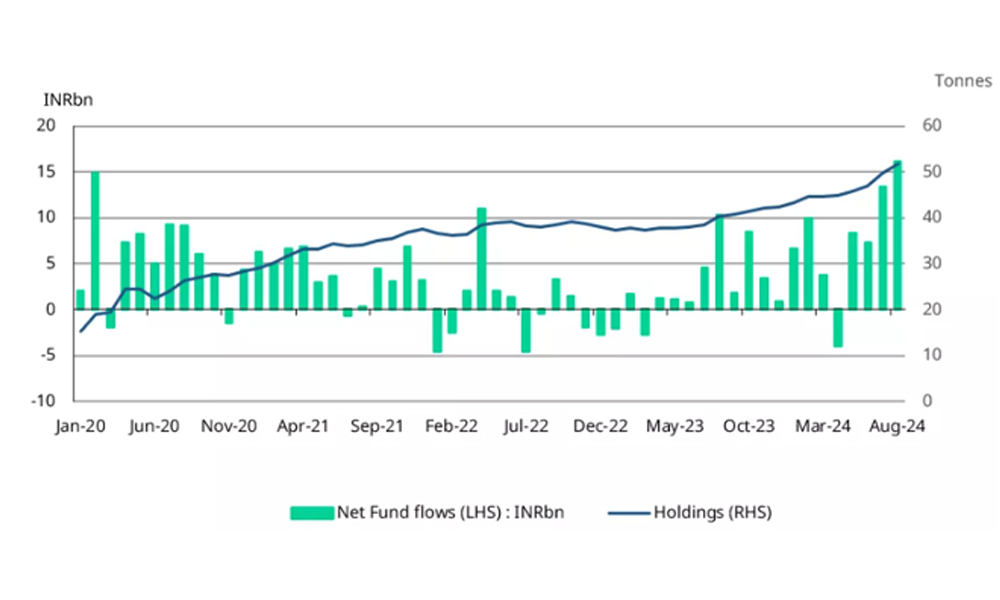

3) Gold ETF Holdings

Investor interest in Indian gold ETF has surged since the end of July. According to AMFI data,

net inflows into Indian gold ETFs have reached Rs 61 billion (~$735 million) thus far in 2024,

a considerable rise of over Rs 15 billion during the same period in the previous year.

Together, these funds have added 9.5tn of gold this year, increasing their total holdings to

51.8tn, a 29% year-over-year rise.

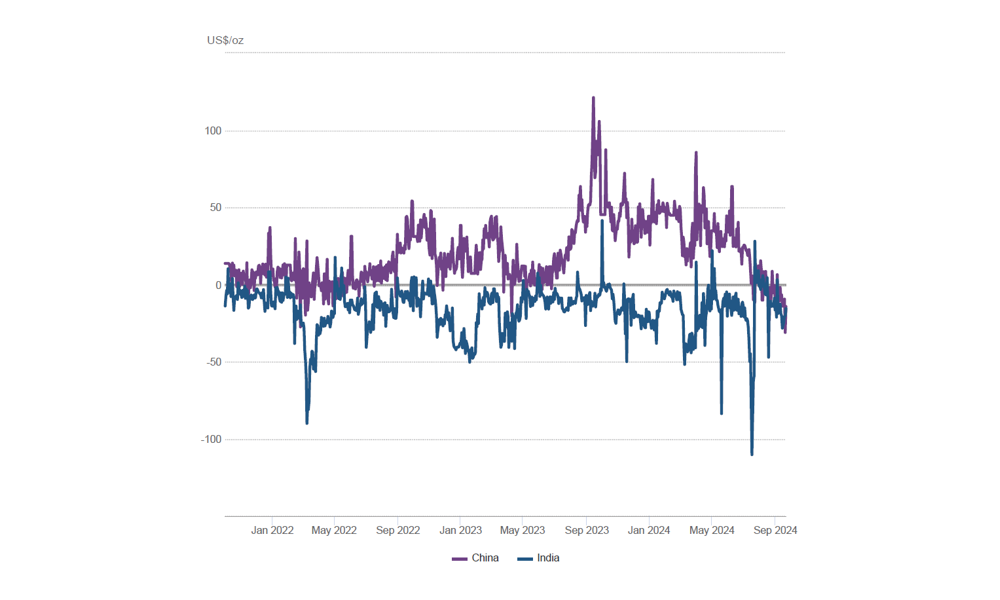

4) Gold Premium/Discount

The gap between domestic and international gold prices has narrowed as a result of rising

global prices and increased supply from increased imports. Domestic gold prices have been

trading either at a modest discount to or in line with international prices in recent weeks,

despite the normalizing but still robust demand.

Diwali Outlook

Overall, with continued global economic uncertainty, gold is expected to retain its appeal

as a hedge against inflation and market volatility. Investors may adopt a “buy on dips”

strategy as the metal is likely to see periodic fluctuations, but the long-term outlook

remains bullish through for next 5-6 months and prices are expected to touch $3000 (~Rs

84000).

Having said that, currently gold prices are in the overbought zone, so we might see a

consolidation phase and a retracement with support at $2575 (~Rs 73000) and resistance

being the next psychological level of $2750 (~Rs 78000) in the next one month.

By Invitation

How seasonal discounts are decisive factors in increasing Jewellery sales

By Shivaram A

Festivals and auspicious occasions are intricately woven into the tapestry of Indian culture and the Indian jewellery trade. Every second month comes up a festival or auspicious occasion and with it comes a downpour of discounts and deals. The Indian customer is ready to lap up the discount offers like milk and honey! So, like other retail businesses, the jewellery retail industry too, depends on seasonal offers and discounts to increase the sales.

Why do seasonal discounts and offers matter?

● The Indian calendar is dotted with festivals and occasions every month. Such festivities are normally associated with jewellery purchase to augur good fortune to the family. To attract customers, offering special festival discounts have become the norm.

● During festivals like Diwali or Pongal, the government employees get their bonus which is a bulk amount used often for investment in gold. To lure the customers to invest heavily in gold purchase, higher discounts are offered.

● Certain auspicious days like Dhanteras or Akshaya Tritiya are specifically linked with gold purchase as families buy gold on these days and worship God with gold coins.

● Occasions like Valentine’s Day, Father’s Day and Mother’s Day are being highlighted recently to push sales further with special offers.

● Certain festivals like Varalakshmi Pooja, Karva Chauth or Vijayadashami have become occasions for women to buy new jewellery. With gold being such a high-priced commodity, frequent purchases are not easy for an average customer. Thus, the only option for a retailer is to offer such discounts and offers during festivals to boost sales.

How to boost jewellery sales using seasonal discounts and offers

- Read your customers Assess the footfall of customers during festive seasons. This

may vary from one shop to another shop in another location depending onthe type of customers you cater to- For example. middleclass customers find it convenient to purchase gold during Diwali, New Year or Akshaya Tritiya. For theaffluent, every day is an occasion.

● The locality your store is in- If your store is located in a North Indian niche, you can expect customers during Dhanteras. In a South Indian locality, Akshaya Tritiya, Onam, Uganda, Pongal, Diwali or Dussehra are the best for buying gold. In a Muslim dominated area, sales are bound to shoot only during weddings. Christians normally purchase gold for their engagements and weddings or during Christmas. Make a list of the days or occasions where you had maximum sales. Some festivals may attract crowds to your store but how many actually bought and why? Analyse.

How seasonal discounts are decisive factors in increasing Jewellery sales

1. Offer a seasonal discount only if it is worth it.

During a festival, every jeweller in town is offering a discount and the competition is intense. Do not just join the competition blindly and offer heavy discounts. Instead, evaluate whether giving a discount of this size has worked for you earlier. If not, you can test-market by offering this discount moderately for a few days and judge the outcome. Offer a seasonal discount only if you think it is worth the trouble. or if you are desperate to liquidate stock.

2. Be different in your discounts

10% off on making charges, zero wastage- all this has become common phrases during festive time. Try something different.

● Tanishq offered a 20% discount on making charges with an additional 5% with State Bank debit and credit cards

● GRT offered silver items free for the weight of gold etc.

● PC Jewellers has cleverly coined its discount deal as “20% off on diamond jewellery” and “20% off on making charges of gold jewellery”. Here the 20% looms large and draws the customer to the store.

● Durga Jewellers of Bangalore goes a step further with its ‘Buy 1, get 2 ” offer on Solitaire jewellery.

3. Make an impact with the discount offer

Evolve print or social media campaigns based on this discountoffer and spread the word around. Intimate your customers of this offer by email, SMS, voice call, WhatsApp or FB messages. Make sure that your discounts make an impact on the customer and draw her to your store. Kamdhenu Jewellers of Chennai has marketed this ad across Facebook and received good response.

4. Special discounts as a mark of loyalty or regular purchase.

Discount depends on your discretion. Turn it into a favourable asset. Yes, it is possible if you offer discounts to

● Loyal customers who have been purchasing jewellery from you for ages, from generation to generation.

● Customers who have brought in many referrals through friends and relatives.

● Frequent shoppers who make small but regular purchases. This not only enhances your customer loyalty but also assures of more purchases in the future years.

The How, When and Why of discounts

It is not just the discount that matters. It is the How, When and Why that matter.

1. How– How do you present your discount? A 20% off on diamond jewellery sounds lame but a Celerio car or an LCD TV sounds huge. The price of both may be equal but, to the customer, yes, the physical representation as a car has great bearing like in this ad.

2. When -When to offer the discount? Offer discounts when your competitors are not even close. Make a difference in the timing of the discount to render it exclusive.

3. Why –Why are you offering the discount? Convey the reason for the discount to the customer- as a

● Festive gift

● Profit-sharing measure

● Mark of the customer’s loyalty.

This will increase the respect and trust among your regular customers. Dishing out discounts, anyone can do. But offering well thought out discounts is the key to successful jewellery retailing.

The world of gemstones is beyond their brilliance, color, transparency, and phenomena. When we think of carvings, we’re not just talking about gemstones used in jewellery. Carving today spans everything from trays and coasters we use every day to idols, vases, and other collectibles that become cherished pieces of art. It’s an often-overlooked art form that deserves recognition for the immense artistry and craftsmanship involved.

As someone deeply embedded in the industry and leading GSI India, I can confidently say that people won’t invest in a piece; no matter how precious the stone: if the carving isn’t done right. So, the first selling point centers around craftsmanship, of course followed by the authenticity and value of the gemstone used.

The quiet poetry of carved gemstones exists beyond the bounds of conventional jewellery design and often go unnoticed in mainstream narratives. Yet they carry some of the richest legacies, the most intimate expressions of craftsmanship, and a cultural gravity that no ideal cut or laser inscription can replicate. Today, as jewellery evolves into a medium of meaning and identity, carved gemstones are experiencing a powerful resurgence. Whether it’s a delicate floral motif on a tourmaline or a symbolic script etched into an emerald, these stones embody permanence with purpose.

For a generation that values intention over ornament, carvings offer exactly that: a wearable emotion, a personal artifact, and a story that transcends carat weight. At GSI, we celebrate jewellery in every form, especially those that carry soul, tradition, and storytelling in their very structure.

From Courts and Temples to Contemporary Studios

Gemstone carving isn’t a trend; it is a tradition. Long before modern jewellery, carved gems were speaking their own language: one of spirit, status, and storytelling. From temple idols to royal signets, they’ve carried meanings deeper than beauty.

Two classical techniques form the backbone of this craft: Intaglios, with designs engraved below the surface for wax seals, and Cameos, where raised motifs emerge in sculptural relief. Both require not just precision, but intuition, a dialogue between artist and stone.

Germany’s Idar-Oberstein remains a living museum of this legacy. Here, stones like agate and jasper are sculpted into heirlooms, passed down as both art and ancestry. Every piece is a story carved in silence.

If Idar-Oberstein is Europe’s carving capital, Jaipur is India’s beating heart. Developed with Mughal patronage particularly by emperors Akbar, Jahangir, and Shah Jahan for their distinguished taste in art, it has since then grown into a global hub; transforming roughs into divine figures, florals, and high fashion commissions. Its edge? A rare blend of old-world mastery and new-world relevance.

And then, there’s Fabergé: the master of turning carving into couture. His works in quartz and chalcedony weren’t just intricate; they were emotional. A blossom. A bunny. A memory in mineral form.

Today, carving is everywhere; from bespoke jewels to vases, coasters, and collectibles. Artists across the world are reimagining tradition for the now. And in an age of instant everything, carved gemstones stand apart: timelessness you can touch, and craftsmanship that speaks with soul.

What the Eye Misses, the Lab Must Find

Carved stones pose a very unique gemological challenge. At our GSI labs, we encounter an extraordinary variety of carved gemstones; each one unique in form, scale, and sentiment. Some are delicately slivered into symbolic motifs, while others are grand in presence, demanding custom instrument setups and careful handling. Testing these pieces, especially when set in jewellery, requires precision, adaptability, and a deep understanding of gemstone behavior.

Carvings, by nature, are emotionally charged. They’re often adored not just for beauty, but for meaning. But emotion must be backed by authentication and the right certification; especially in today’s high-value, high-stakes market. Whether it’s identifying treatments, or distinguishing natural from imitations, our role is to bring clarity to complexity.

At GSI, we don’t just verify a gemstone; we translate its unspoken story. From the delicate depths of an intaglio to the elevated relief of a cameo, our certification doesn’t just protect value; it protects legacy.

Technology Has Unlocked New Possibilities

Modern lapidaries are now able to carve harder materials with precision that was once unthinkable. For a long time, artists chose softer, more affordable stones, to avoid breakage, and preserve weight. Using precious gems was simply too risky. But with time and technology, that’s changed. Today, gem material like sapphire, spinel, and topaz, once considered too delicate to sculpt, are being carved with remarkable precision. What was once unthinkable is now part of the craft’s evolving canvas.

But while tools evolve, the soul of carving stays rooted in intention, vision, and a deep respect for the stone’s natural voice. That interplay between human and mineral is what makes a carving come alive.

Today, luxury is no longer defined by price tags or perfection alone; it’s about meaning, craftsmanship, and cultural richness. Carved gemstones carry all of that, and more.

At GSI, we believe that true appreciation begins with understanding. Whether it’s a carved idol, a custom tray, or a fine piece of jewellery, the value of a gemstone lies in both its beauty and its authenticity. That’s why certification matters: not just for what a gem is, but for the story it tells.

By Invitation

Mangalsutra Market Glows with Steady 11% Growth rate

By Tanvi Shah- Director & Head – CareEdge Advisory & Research

The gems and jewellery market has clocked a healthy CAGR of 11% from CY20-24, to reach at Rs. 8,110 billion in CY24. A similar growth trajectory is expected to continue in the next 5 years. Furthermore, bangles and chains hold a large share in the overall jewellery market. As consumer preferences evolve, the Indian jewellery sector is undergoing notable transformation. Central to this shift is the Mangalsutra—a piece that embodies both cultural heritage and modern sensibility. Traditionally revered as a symbol of marital unity and prosperity, the Mangalsutra has maintained its cultural significance while aligning with contemporary aesthetics and changing lifestyles.

The Mangalsutra market has grown at over 10% compounded annual growth rate (CAGR) over the past five years and estimated to be Rs 190 billion in CY24(E). With the consistently rising number of weddings in India, the market is set to expand steadily and is expected to surpass Rs 250 billion by CY29.

Weddings: The Prime Driver of Demand

Weddings remain the key driver of Mangalsutra purchases, with the ornament continuing to symbolize matrimony across communities. As weddings evolve—especially with greater financial independence among millennial couples—buying behaviours are also shifting. While 80–82% of wedding expenses are still covered through savings, around 10% rely on loans and 6–8% liquidate assets.

In 2024, India recorded 124.3 lakh weddings, marking a strong post-pandemic momentum. This upward trend continued from earlier years and is expected to accelerate, with weddings projected to reach 180.8 lakh by 2032, registering a CAGR of 4.8%. This growth is also fuelling demand for bridal jewellery, underscoring the wedding sector’s resilience and its rising contribution to the national economy.

Chart 1: Total Number of Weddings in India, CY2024-32

Source: Industry Sources, CareEdge Research

Source: Industry Sources, CareEdge Research

The rise of destination weddings and thematic ceremonies has prompted demand for multiple Mangalsutra designs. Brides now seek elaborate gold pieces for traditional rituals and minimalist styles for more modern or informal functions. This shift has encouraged jewellers to diversify their offerings, enabling repeat purchases beyond the initial wedding.

Evolving Designs: A Fusion of Style and Sentiment

Although traditional Mangalsutras—characterised by black beads and gold links—continue to dominate, capturing a 62% share of the market in CY24, the preference for modern alternatives is rising. Designs featuring sleek lines, diamonds, and mixed metals now comprise 32% of the market and resonate particularly with younger, urban consumers who prioritise versatility and style.

Chart 2: Indian Mangalsutra Market: Break-up by Design (% share) for CY24(E)

Customisation has emerged as a notable trend. Consumers increasingly request bespoke elements, including unique pendant shapes, gemstone settings, and tailored chain lengths. Presently, customised Mangalsutras account for approximately 5% of the market. Jewellers are responding by embracing advanced design technologies and personalised consultations, enabling them to cater to diverse tastes and preferences.

Material Preferences Reflect Shifting Choices considering prices

Gold remains the market leader in Mangalsutra, and 22K gold accounts for 52% of the share because of its long-standing tradition of symbolizing security and affluence. Nevertheless, an price increase—from around Rs 67,175 per 10 grams during April 2024 to Rs 90,050 as of 24th April 2025—has forced consumers to question their decisions, tending towards lighter or affordable options.

Chart 3: Indian Mangalsutra Market Breakup by Material Type (% share) for CY24(E)

Source: CareEdge Research

Note: Others include Beads, Synthetic Metals, Semi-Precious stones, etc.

Silver Mangalsutras, now commanding a 31% share, offer an affordable and wearable alternative. Their simplicity appeals to younger consumers who seek practical, everyday options. Meanwhile, diamond Mangalsutras hold a 12% market share, gaining popularity among those who value elegance and symbolic distinction. Fusion designs, incorporating gold, silver, and diamonds, are also gaining ground as jewellers strive to serve a broader demographic.

Market Outlook: Strong Sentiment supporting healthy Sales Growth

Gold Mangalsutras continue to represent nearly 52.3% of the total market, but interest in alternative silver or diamond variants is also attracting more consumers. Going forward, these changing consumer preferences will encourage many new replacement and repeat purchases, creating fresh opportunities for jewellers.

In contrast to the overall demand for gold jewellery, which declined by 2.3 percent year-on-year in CY24, the Mangalsutra market demonstrated remarkable resilience by maintaining double-digit growth. As weddings continued and consumer preferences evolved, the Mangalsutra adapted accordingly embracing new and exciting designs without compromising its cultural significance.

A commitment symbol and a personal style will keep it constantly relevant in India’s jewellery landscape, full of diversity and dynamism.

ALROSA’s Severalmaz ramps up output as Karpinsky-2 diamond pipe enters development

PC Jeweller Soars 33% in Two Days on Strong Q1 Revenue Growth and Debt Reduction Plans

Senco Gold Q1 Revenue Jumps 28% on Festive Demand and Store Expansion

ALROSA’s Severalmaz ramps up output as Karpinsky-2 diamond pipe enters development

PC Jeweller Soars 33% in Two Days on Strong Q1 Revenue Growth and Debt Reduction Plans

Senco Gold Q1 Revenue Jumps 28% on Festive Demand and Store Expansion

-

National News5 days ago

National News5 days agoMalabar Gold & Diamonds Inaugurates Landmark Integrated Manufacturing Site in Hyderabad, Cementing Its Position as a Global Manufacturing Leader

-

National News2 months ago

National News2 months agoEmmadi Silver Jewellery Launches First Karnataka Store with Grand Opening in Bengaluru’s Malleshwaram

-

BrandBuzz3 months ago

BrandBuzz3 months agoMia by Tanishq Unveils ‘Fiora’ Collection This Akshaya Tritiya: A Celebration of Nature’s Blossoms and New Beginnings

-

GlamBuzz2 months ago

GlamBuzz2 months agoGokulam Signature Jewels Debuts in Hyderabad with Glamorous Launch at KPHB