International News

WGC Gold Market Commentary: Bonds a no go

A staggering 14% rally in January took gold above the US$5,000 mark, cementing the 5k number as a headline to match the first recorded annual 5,000 tonnes of total demand. The month closed at US$4,982/oz and scored 12 all-time highs. But it was not without drama with large intraday swings on the last two days of the month.

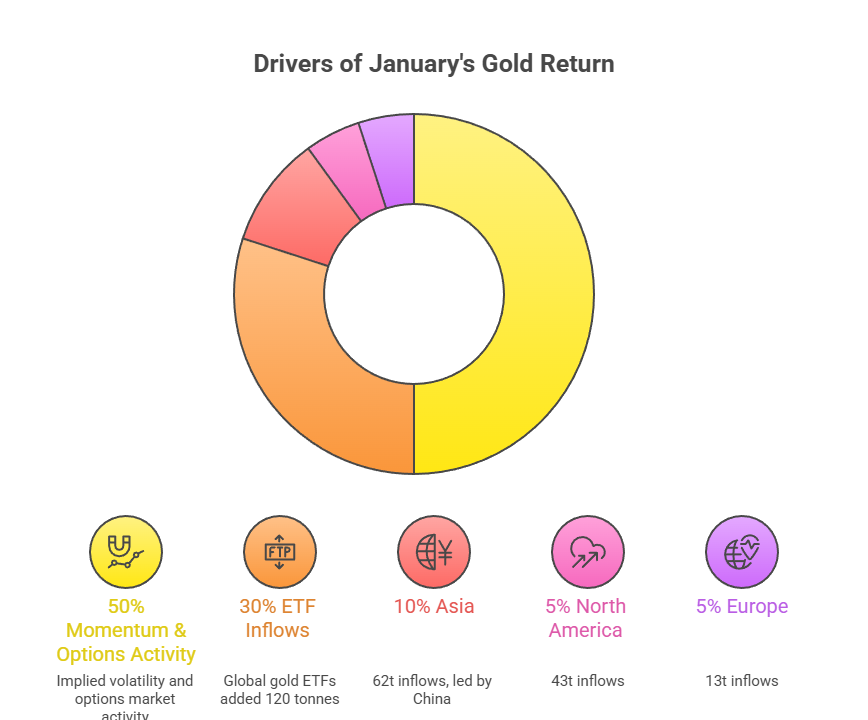

Our Gold Return Attribution Model (GRAM) showed an unusually large contribution from implied volatility (c.50% of January’s return), reflecting substantial option market activity. This variable currently sits in risk & uncertainty, although is likely more reflective here of momentum.

Global gold ETF flows provided plenty of support adding 120t in January to take holdings to a new record, valued at US$669bn. The flows were dominated by Asia (62t) and North America (43t) while Europe saw more modest inflows

Key Price Figures (January 2026)

The month was characterized by relentless momentum, scoring 12 all-time highs before ending with significant intraday volatility.

| Metric | Value (USD) | Peak Date |

| January Closing Price | US$4,982/oz | Jan 30, 2026 |

| All-Time Record High | US$5,307/oz | Jan 28, 2026 |

| Monthly Return | +14.1% | — |

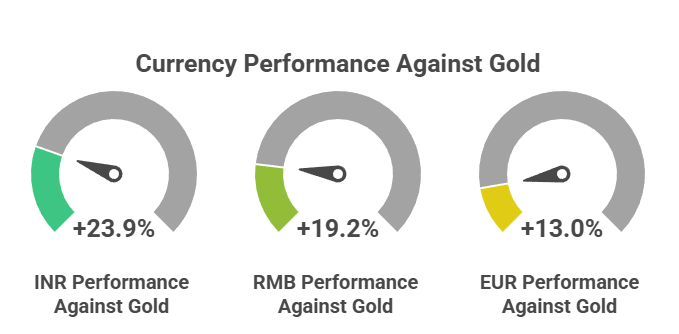

Performance in Other Major Currencies (Jan Return):

- INR: +23.9% (Record high: ₹176,306/10g)

- RMB: +19.2% (Record high: ¥1,248/g)

- EUR: +13.0% (Record high: €4,444/oz)

Major Market Drivers

- Momentum & Options (GRAM Model): Approximately 50% of January’s return was attributed to implied volatility and massive options market activity rather than pure macro fundamentals.

- ETF Inflows: Global gold ETFs added 120 tonnes (valued at US$669bn), the strongest month on record.

- Asia: 62t (led by China)

- North America: 43t

- Europe: 13t

- The “Warsh Effect”: Late-month drama was fueled by the nomination of Kevin Warsh as the next Fed Chair. Markets perceive him as a “hawk” favoring a smaller Fed balance sheet, which triggered a sharp intraday correction from the $5,300 peaks.

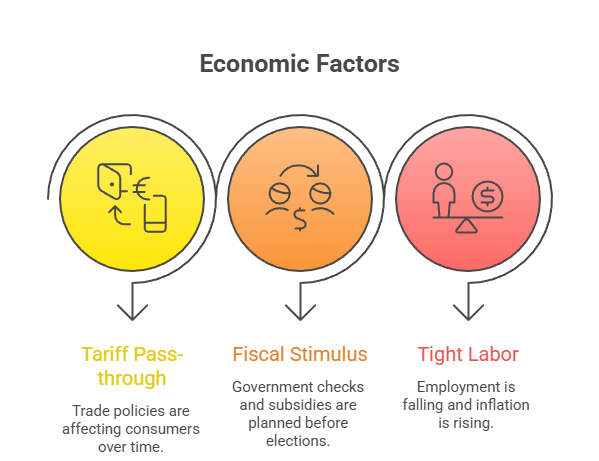

Macro Outlook: The Inflation Resurgence

While geopolitics dominated January, the narrative is shifting toward resurgent US inflation risks for the remainder of 2026. Key triggers include:

- Tariff Pass-through: Lagged effects of trade policies hitting consumers.

- Fiscal Stimulus: Prospective $2,000 “tariff dividend” checks and ACA subsidies ahead of the US mid-term elections.

- Tight Labor: A falling breakeven employment rate and rising household inflation expectations.

Investment Implications

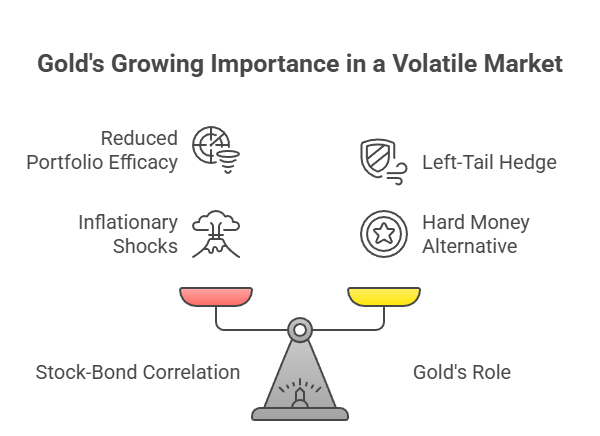

- Stock-Bond Correlation: Inflationary shocks are making stocks and bonds move in the same direction, reducing the efficacy of traditional 60/40 portfolios.

- Gold’s Role: Gold is increasingly viewed as a left-tail hedge and a “hard money” alternative as sovereign debt levels (reaching 30% of the $340T global sector debt) raise debasement fears.

The gold market is likely to “pause” after the January surge, but the combination of fiscal expansion and Fed leadership uncertainty suggests investment demand will remain a structural feature of 2026.

source :WGC

International News

Payrolls Shock Reshapes Fed Bets, Sends Bullion Sharply Higher AUGMONT BULLION REPORT

Bullion’s Strongest Week: Gold Up 6.6% To ~$4,350; Silver Surges Nearly 7% To $65.05

Bullion had one of its strongest weeks of the year. Spot gold climbed roughly 6.6% to settle near $4,350/oz, with COMEX December futures touching an intraday high above $4,410 before easing into the close. Silver outperformed on a percentage basis, with spot prices vaulting from the high-$50s to an intraday peak of $65.05/oz, a gain of nearly 7%.

The U.S. economy lost 23,000 jobs in July, the Labor Department said, compared with economists’ expectations for an increase of 80,000 jobs, according to a Reuters poll. The unemployment rate fell to 4.1% even as the labor participation rate dropped to a near five-and-a-half-year low of 61.4%. Few expected non-farm payrolls to turn negative, or that June’s numbers would see such a steep downward revision.

The market has likely pushed the expected Fed hike from September to October or December, Wizman said, noting that weak labor data tends to delay rate-hike expectations rather than accelerate them. ADP’s weekly employment data had already pointed to a hiring slowdown earlier in the week, setting up the payrolls shock. With CPI, PPI, and University of Michigan inflation expectations due shortly, markets remain highly sensitive to incoming data, and positioning into next week is expected to stay volatile. Fed funds futures traders are now pricing in 44% odds of a rate hike at the September meeting, down from 55% before the data.

Safe-haven flows got extra support from unresolved tensions around the Strait of Hormuz. Reports suggested Iran and Oman were negotiating an arrangement to ease shipping disruptions, though no final agreement was confirmed, and crude oil pulled back from recent highs on partial de-escalation optimism. Without a durable resolution, a geopolitical risk premium stayed embedded in both gold and silver through the week, while a coordinated US-Japan currency intervention to steady the yen added another layer of cross-asset volatility that spilled into precious metals positioning.

Domestic sentiment stayed constructive heading into the festive and wedding season window that opens in August. Feedback from recent trade events pointed to improved restocking by jewellers, though record rupee prices continue to push consumers toward lighter-weight, lower-carat pieces and value-conscious purchases. Investment demand through coins, bars, and gold ETFs continued to outpace jewellery offtake, in line with the broader shift in Indian consumer behavior toward gold as a financial-security instrument rather than a purely occasion-led purchase.

With US CPI, PPI, jobless claims, and Michigan sentiment data on the calendar, volatility is likely to stay elevated. Gold holding above the $4,200–4,350 zone will be key to sustaining the advance toward record territory, while silver’s move above $63 keeps the door open for a retest of the January highs if the dollar stays under pressure.

Gold and silver appear to have formed a base and broken out after a month-long consolidation, so a 4–5% upside move looks likely this week. On MCX, Rs 1,40,000 is the immediate support band for gold, with silver support near Rs 2,15,000–2,20,000. A confirmed Fed dovish pivot, alongside any durable Strait of Hormuz resolution, will be the swing factors for direction into the following week.

GJC Announces 15th Edition Of National Jewellery Awards – Celebrating Excellence & Innovation

Shankesh Jewellers Limited’s Initial Public Offering To Open On Tuesday, August 18, 2026

Jos Alukkas Unveils Exclusive Onam Offers Across Kerala

GJC Announces 15th Edition Of National Jewellery Awards – Celebrating Excellence & Innovation

Shankesh Jewellers Limited’s Initial Public Offering To Open On Tuesday, August 18, 2026

Jos Alukkas Unveils Exclusive Onam Offers Across Kerala

-

National News11 hours ago

National News11 hours agoGJC Announces 15th Edition Of National Jewellery Awards – Celebrating Excellence & Innovation

-

National News11 hours ago

National News11 hours agoShankesh Jewellers Limited’s Initial Public Offering To Open On Tuesday, August 18, 2026

-

National News12 hours ago

National News12 hours agoJos Alukkas Unveils Exclusive Onam Offers Across Kerala

-

New Premises1 day ago

New Premises1 day agoPNG Launches The Flagship Store Of YOOU, A Brand Around Evolving Identities Of Modern Women