International News

China’s Diamond Market Undergoes Dramatic Recalibration

Once a powerhouse of global luxury demand, China’s diamond market is experiencing a profound transformation, reflecting both changing consumer values and evolving economic realities. Liang Weizhang, CEO of HubWis Jewellery Strategic Creations (Guangzhou) Co., Ltd., provides an in-depth analysis of the latest trends, underlying drivers, and strategic imperatives for the industry.

According to the Gems & Jewelry Trade Association of China, the diamond market shrank from RMB 100 billion in 2021 to RMB 43 billion in 2024-a 57% drop-while diamonds’ share of the overall jewelry market fell from 14% to 6%. This contraction stands in stark contrast to the sector’s previous rapid expansion, but signals not just a downturn, but a realignment of consumer priorities and market structures.

While diamond demand has cooled, gold jewelry has surged, increasing its market share from 58% to 73% between 2021 and 2024. Other segments, such as jade and pearls, have seen volatility. Despite these shifts, the total Chinese jewelry market remains resilient, growing from RMB 720.5 billion in 2021 to RMB 820 billion in 2023, before a modest dip to RMB 778.8 billion in 2024. This underscores a rebalancing across categories rather than a wholesale decline in jewelry demand.

Customs data reveal a 73% drop in the volume of gem-quality diamond imports between 2021 and 2024, with import values plummeting 83%. Even as the volume of imports fell only 4% year-on-year in 2024, the value declined 40%, indicating significant downward pressure on prices and a shift toward more affordable, differentiated products.

Millennials and Gen Z are redefining luxury, prioritizing individuality, ethical sourcing, and value. For many, diamonds are now one of many ways to express personal identity rather than the ultimate status symbol. The rapid rise of laboratory-grown diamonds-offering sustainability and affordability-has further diversified the market, challenging the dominance of natural stones.

China’s moderated GDP growth and declining marriage rates have dampened demand for traditional diamond jewelry, particularly engagement rings. Consumers are increasingly drawn to gold, which offers both adornment and investment value, while diamond brands must work harder to connect emotionally and symbolically with buyers.

Industry leaders caution against viewing the contraction as permanent. Instead, they advocate for differentiated offerings, stronger storytelling, and digital engagement. Regional diversity within China presents growth opportunities, especially in emerging cities with distinct consumer profiles. Early signs of stabilization-such as increased activity at the Hong Kong Jewellery Show-offer cautious optimism for a gradual recovery.

International News

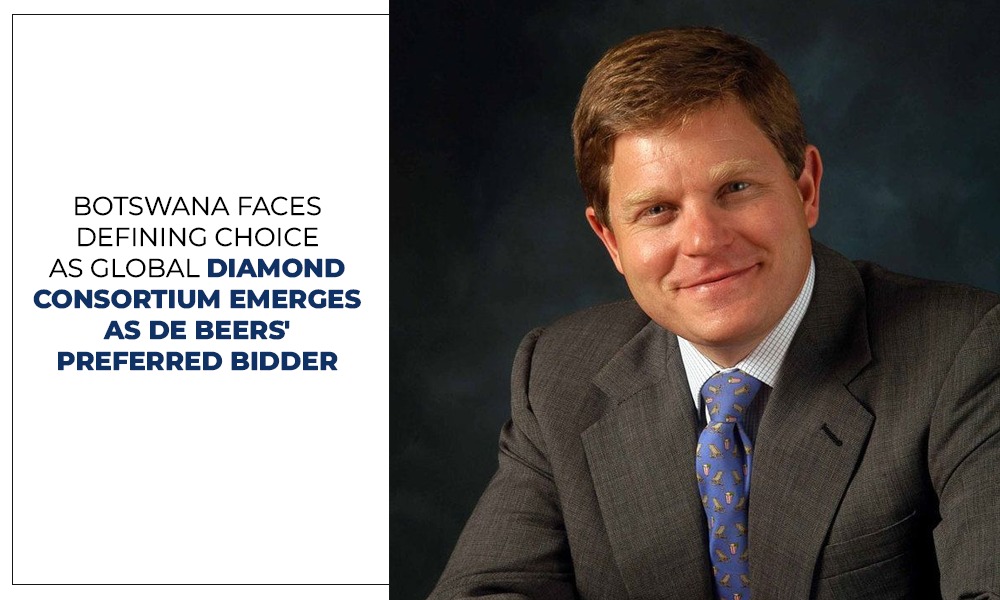

Consortium Led By Former De Beers CEO Gareth Penny Selected As The Preferred Bidder To Acquire De Beers

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers

A consortium headed by former De Beers CEO Gareth Penny has been selected as the preferred bidder to acquire De Beers, according to Botswana’s Minister for State President, Defence and Security, Moeti Mohwasa.

Speaking on the development, Mohwasa said Anglo American conducted a competitive sale process involving three shortlisted bidders before identifying the Global Diamond Consortium as its preferred choice.

Anglo American announced plans to divest De Beers in May 2024 as part of a broader restructuring strategy, driven by prolonged weakness in the diamond market and other business priorities.

The sale process has attracted significant interest from industry leaders and investors. Among those previously linked to the bidding were former De Beers CEO Bruce Cleaver, Australian mining executive Michael O’Keeffe, Indian billionaire Anil Agarwal, and Indian diamond companies KGK Group and Kapu Gems.

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers and retains important rights under the shareholder agreement. Mohwasa emphasized that Botswana has the flexibility to either join the preferred bidder as a strategic partner or exercise its pre-emptive rights independently or with another investor.

Industry observers believe the eventual owner will seek to preserve De Beers’ vertically integrated business model, spanning diamond mining, trading and global natural diamond marketing, while positioning the company to benefit from a potential recovery in natural diamond demand and prices.

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

FIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

-

BrandBuzz19 hours ago

BrandBuzz19 hours agoFIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

-

National News18 hours ago

National News18 hours agoNature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

-

New Premises17 hours ago

New Premises17 hours agoVinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

-

National News15 hours ago

National News15 hours agoRajiv Jain Elected Chairman Of Jaipur Jewellery Show