JB Insights

WGC Gold Demand Trends : Gold breaks records as investors seek shelter from market turbulence

The World Gold Council’s Q3 2025 Gold Demand Trends report reveals that quarterly gold demand (including OTC) reached 1,313t, or US $146bn in value terms and was the highest quarter for demand on record.

Growth was driven primarily by investment demand which accelerated in Q3 reaching 537t (+47% y/y) and accounted for 55% of overall net gold demand. This momentum was driven by a powerful combination of an uncertain and volatile geopolitical environment, US dollar weakness and investor “FOMO” as the price climbed higher.

Investors continued to pile into physically backed gold ETFs for a third consecutive quarter, adding a further 222t with global inflows reaching US$26bn. Year-to-date, gold ETFs have added a total of 619t (US$64bn) to their holdings with North American listed funds leading the charge (346t), followed by European (148t) and Asian funds (118t).

Bar and coin investment rose 17% y/y, totalling 316t, with growth in almost all markets but with significant contributions from India (92t), China, (74t).

On the other hand, gold jewellery demand was weighed down by 50 record gold prices this year, seeing a 19% y/y decline in consumption for Q3. While the two largest consumer markets – India and China – both saw a quarter-on-quarter uplift, largely due to seasonal factors, the y/y picture across both markets remained weak.

Central banks picked up the pace in Q3 with net purchases totalling 220t in the third quarter, up 28% on Q2 and 10% y/y, despite the record-high gold price. On a year-to-date basis, net buying totalled 634t, trailing behind the exceptional highs of the last three years, but comfortably above pre-2022 levels.

Total gold supply reached a quarterly record of 1,313t, up 3% y/y. Mine production increased by 2% y/y to 977t while recycling was up 6% y/y at 344t, staying relatively stable given the soaring gold price.

Louise Street, Senior Markets Analyst at the World Gold Council, commented:

“Gold’s climb towards US$4,000/oz in the third quarter underscores the strength and persistence of the factors that have been driving demand throughout the year. Heightened geopolitical tensions, stubborn inflationary pressures and uncertainty around global trade policy have all fuelled appetite for safe-haven assets as investors look to build resilience in their portfolios.

“The outlook for gold remains optimistic, as continued US dollar weakness, lower interest rate expectations, and the threat of stagflation could further propel investment demand. Gold has set record after record this year, and the current environment suggests there could be more upside gains for gold. Our research indicates the market is not yet saturated, and the strategic case to hold gold remains firmly in place.”

Sachin Jain, Regional CEO, India, World Gold Council said:

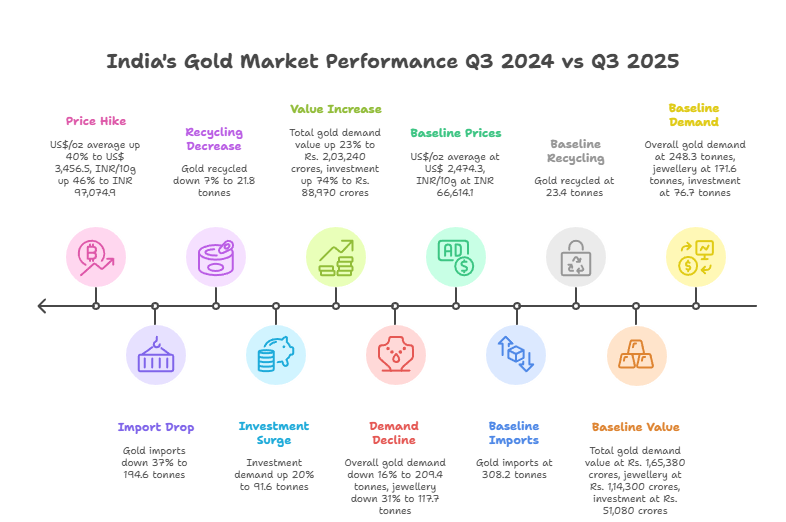

“India’s gold market in Q3 2025 showcased its inherent resilience and the significant impact of evolving price dynamics. While total gold value surged impressively by 23% to Rs. 2,03,240 crores, gold demand volumes saw a 16% decline to 209.4 tonnes. This robust growth in value, driven by high average prices, strongly reaffirms gold’s enduring appeal as a safe-haven asset. Investment demand, showed remarkable strength, increasing 20% in volume to 91.6 tonnes and a significant 74% in value to Rs. 88,970 crores.

This highlights a deepening strategic commitment among Indian consumers to gold as a long-term store of value. While jewellery demand saw a 31% volume decrease to 117.7 tonnes, its value remained largely stable at Rs. 1,14,270 crores. This indicates that despite higher prices, gold’s intrinsic cultural significance continues to drive purchases, with consumers adapting to the new price levels.

On the supply side, gold imports were 194.6 tonnes, down 37%, while recycling saw a modest 7% decline to 21.8 tonnes, suggesting consumers are holding onto their prized asset. Looking ahead, the current festive and wedding seasons are pivotal for the yellow metal. Gold’s unique cultural significance means festivals traditionally drive strong buying interest. Despite prevailing high prices, consumer sentiment remains positive, and retailers are well-prepared. We anticipate robust demand across all categories, from traditional jewellery to investment products, as the market gears up for a vibrant festive and wedding season. With total gold demand from January to September at approximately 462.4 tonnes, we anticipate full-year demand between 600 and 700 tonnes, more towards higher end of range.“

Gold Demand Trends Q3 2025 India Fact Sheet: India Gold Demand Statistics for Q3 2025 (July – September)

- Demand for gold in India for Q3 2025 was at 209.4 tonnes, down by 16% as compared to overall Q3 demand for 2024 (248.3 tonnes)

- India’s Q3 2025 gold demand value was Rs. 2,03,240 crores, up by 23% as compared to Q3 2024 (Rs.1,65,380 crores)

- Total Jewellery demand in India for Q3 2025 decreased by 31% to 117.7 tonnes as compared to Q3 2024 (171.6 tonnes)

- The value of jewellery demand remained rather unchanged at Rs. 1,14,270 crores, compared to Rs. 1,14,300 crores recorded in Q3 2024

- Total Investment demand for Q3 2025 was at 91.6 tonnes, increased by 20% in comparison to Q3 2024 (76.7 tonnes)

- In value terms, gold Investment demand in Q3 2025 was Rs. 88,970 crores, up by 74% from Q3 2024 (Rs. 51,080 crores)

- Total gold recycled in India in Q3 2025 was 21.8 tonnes, down by 7% compared to 23.4 tonnes in Q3 2024.

- Total gold imports in India in Q3 2025 was 194.6 tonnes, down by 37% compared to 308.2 tonnes in Q3 2024.

- US$/oz average quarterly price in Q3 2025 was US$ 3,456.5 in comparison to US$ 2,474.3 in Q3 2024.

- INR/10g average quarterly price in Q3 2025 was INR 97,074.9 in comparison to INR 66,614.1 in Q3 2024 (without import duty and GST)

JB Insights

The Woman Wearing The Diamond Was Never The One The Ad Was Talking To

Disha Shah, Founder & Designer, DiAi Designs Says That The Brands That Shift From “She Deserves It” to “She Chose It” Won’t Just Win Cultural Relevance – They’ll Own The Future Of Jewellery Marketing.

Indian jewellery advertising has always centred the woman. She has been the face of every campaign, draped in gold, luminous at the occasion, receiving the gift with practised grace. What she rarely was, until recently, was the intended audience.

The creative language of the category was built around a genuine economic reality. For decades, the buyer in Indian fine jewellery was the patriarch, the husband, the father, the family elder making a financial decision on behalf of a woman whose purchasing autonomy was limited. Advertising followed the money. The gift reveal, the bridal close-up, the family approval shot: these were not arbitrary creative choices. They reflected who held the purse strings, and they became so embedded in the category’s visual grammar that they outlasted the conditions that created them by an entire generation.

That structural reality has now reversed. Jewellery purchases now extend beyond weddings and festivals to daily wear, driven by financially independent working women. The self-purchasing woman is no longer an emerging segment; she is the category’s fastest-growing buyer, approaching the decision differently from the buyer the industry originally designed itself around. She is not waiting for an occasion. She is not waiting for someone to present a box. She researched the piece, chose it, and bought it because she wanted it.

The advertising, for the most part, has not caught up.

Some brands are beginning to recognise this. CaratLane’s #WearYourWins movement and Tanishq’s sustained push toward the “woman as decision-maker” are meaningful steps. But what makes these campaigns commercially smart is not just cultural alignment. Research from Harvard Business School finds that women systematically provide less favourable assessments of their own performance and potential than equally performing men. This documented self-promotion gap persists even when women know they have outperformed others. Campaigns that actively celebrate female self-recognition are not just filling a creative gap. They are responding to a behavioural reality that has gone largely unaddressed in the category. The brands doing this well are not being progressive for their own sake. They are being accurate about who their buyer is and what she needs to hear.

Look at the Women’s Day 2026 campaigns across the industry. The conversation is clearly starting to pivot. Brands are finally stepping away from the usual gifting tropes and reframing jewellery as a tool for personal milestones and self-expression. But these remain exceptions. The dominant campaign language of Indian jewellery- the gesture, the reveal, the woman being seen rather than deciding- has not structurally changed.

The media mix tells the same story. Titan leaned heavily on television in FY25, with ad volume surging to 77% of its mix, a broadcast medium built for household reach rather than the individual, financially independent woman who now represents the category’s fastest-growing buyer.

Meanwhile, digitally native BlueStone achieved 50% of online jewellery ad volumes on a budget nearly ten times smaller than Titan’s. The channel that reaches the self-purchasing woman directly is delivering outsized results on a fraction of the spend. The implication for where the industry should be directing its creative attention is fairly clear.

Consider what a brief genuinely written for this buyer would look like. No occasion in the shot. No second person in the frame presents anything. The opening line is not “for the woman who deserves to be celebrated.” It is “she saw it, she wanted it, she bought it.” The product earns its place not through sentiment but through desire. The copy does not explain why she is worth it. It assumes she already knows. That is not a tonal adjustment. It is a fundamentally different creative architecture, and very few briefs in this category have been written that way.

The LGD category has a specific opportunity here that established houses do not. Without decades of legacy campaign language to protect, an independent designer in this space can build advertising from a blank page, one written entirely around the woman who is actually making the purchase. The brief does not have to accommodate inherited assumptions about who the buyer is or what she is waiting for. That is not a small advantage. In a category where the dominant creative language was built around a buyer who is no longer the one making the decision, starting without that inheritance may be the most powerful creative position available.

The woman wearing the diamond has always been visible. What is changing now is who gets to decide. The brands that build their creative around that reality will not just be more culturally relevant. They will be better positioned for every year that follows. The advertising has not caught up yet. But the buyer already has.

The Titanium Jewellery Manufacturing:Convergence Of Advanced Manufacturing, AI, and Surface Chemistry

IAGES Accredited Partner Directory Brings Verified Gold Businesses Together on One Trusted Platform

De Beers Group Sets Out Portfolio and Organisational Actions to Support Long-Term Value Creation

The Titanium Jewellery Manufacturing:Convergence Of Advanced Manufacturing, AI, and Surface Chemistry

IAGES Accredited Partner Directory Brings Verified Gold Businesses Together on One Trusted Platform

Jagannath Gangaram Pednekar Jewellers Unveils ‘The Godhadi Effect’, A Heartfelt Film Reimagining Gold Exchange Through Family Memories

-

TechBuzz54 minutes ago

TechBuzz54 minutes agoThe Titanium Jewellery Manufacturing:Convergence Of Advanced Manufacturing, AI, and Surface Chemistry

-

National News18 hours ago

National News18 hours agoIAGES Accredited Partner Directory Brings Verified Gold Businesses Together on One Trusted Platform

-

BrandBuzz20 hours ago

BrandBuzz20 hours agoJagannath Gangaram Pednekar Jewellers Unveils ‘The Godhadi Effect’, A Heartfelt Film Reimagining Gold Exchange Through Family Memories

-

GlamBuzz20 hours ago

GlamBuzz20 hours agoGargi Of P N Gadgil and Sons Launches 2026 Monsoon Collection With Brand Ambassador Mithila Palkar