DiamondBuzz

Botswana Diamonds rebrands as Botswana Minerals PLC

Signals a definitive shift toward copper exploration as the diamond market faces a stiff cyclical downturn.

Botswana Diamonds PLC, a long-time explorer of the world’s most famous gemstones, has officially rebranded as Botswana Minerals PLC, signaling a definitive shift toward copper exploration as the diamond market faces a stiff cyclical downturn. The name change, which took effect Feb. 27, follows a strategic review that leveraged artificial intelligence to scan the company’s massive 95,000-square-kilometer geological database. While the AI was originally designed to hunt for kimberlite pipes—the volcanic rock that hosts diamonds—it instead unearthed “outstanding” evidence of copper deposits.

A High-Tech Pivot

The company, listed on London’s AIM and the Botswana Stock Exchange, has identified 11 copper targets across the country and has already secured eight prospecting licenses. The move reflects a broader trend among junior miners seeking to capitalize on the “green metal” boom driven by electric vehicles, renewable energy, and AI data centers.

The Diamond Dilemma

The rebranding comes as the natural diamond sector grapples with two simultaneous concerns:

- Technological Disruption: Lab-grown diamonds continue to cannibalize the lower end of the market, offering consumers a cheaper alternative that is chemically identical to mined stones.

- Cyclical Downturn: Sluggish global demand and high inventory levels have dampened investor enthusiasm for natural stones.

Despite the pivot, the company is not abandoning its roots entirely. It remains one of the largest holders of exploration data in Botswana and intends to maintain its diamond acreage, betting that high-quality natural stones will eventually regain their luster.

By shifting focus to copper, Botswana Minerals (trading under the new ticker BMIN) joins a growing list of players in the Kalahari Copper Belt, a region increasingly viewed as a world-class mining frontier.

DiamondBuzz

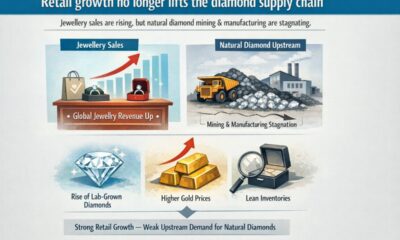

Despite revenue growth in jewellery sector, natural diamond upstream sees stagnation

Lab-grown disruption, soaring gold prices and leaner retail inventories decouple jewellery revenue growth from natural diamond mining and manufacturing demand

Despite robust revenue growth in the global jewellery sector, the natural diamond upstream (mining and manufacturing) is facing stagnation due to a fundamental shift in product mix and inventory strategy. Jewellery sales are rising across key markets, but a shift toward lab-grown stones, higher gold prices and leaner inventories means that growth at the counter is no longer translating into stronger demand for natural diamonds upstream.

Market Performance vs. Natural Diamond Demand

- Strong Retail Indicators: Major luxury conglomerates and commercial retailers reported significant YOY revenue growth (e.g., Richemont +6%, Titan Company +24%, Chow Tai Fook +18%).

- The Disconnect: While total jewellery revenue is rising, the natural diamond component of that revenue is shrinking. Diamonds now represent ~41% of total jewellery sales, down from 50% a decade ago.

Primary Drivers of Structural Disruption

- Market Share Erosion by Lab-Grown Diamonds (LGDs):

-

- LGDs have achieved dominant penetration in the bridal segment (61% of US engagements in 2025).

- Retailers are actively “leading” with LGDs, diverting unit volume away from natural stones.

- Segment Squeezing & Substitution:

- Consumers are opting for larger LGDs at price points previously reserved for 0.50–1.50 carat natural stones.

- This has hollowed out the “mid-market” natural diamond category, forcing upstream demand toward only the highest-value, large stones.

- Commodity Price Pressure (The Gold Factor):

-

- Surging gold prices have absorbed a larger share of the consumer’s total “per-piece” budget.

- Design Engineering: Manufacturers are reducing diamond counts or using smaller accent stones to maintain price points, leading to lower natural diamond volume per SKU.

Supply Chain & Distribution Evolution

- Retail Consolidation: The US market is seeing a 2%–3% annual decline in the number of jewellery businesses (JBT data). A smaller retail footprint naturally results in fewer aggregate “stocking orders.”

- Lean Inventory Management: * Transition from “Just-in-Case” to “Just-in-Time” replenishment models.

Retailers are maintaining tighter stock levels due to volatile pricing and high credit costs, buying only against confirmed consumer demand rather than speculative inventory building.

The New Normal for Upstream Stakeholders

The traditional “bullwhip effect” that previously benefited miners and manufacturers has been dampened. Growth at the retail counter no longer guarantees a surge in the midstream. The natural diamond supply chain must now realign for a lower-volume, higher-value environment until natural stones can reclaim a distinct value proposition relative to LGDs and gold-heavy designs.

-

DiamondBuzz1 hour ago

DiamondBuzz1 hour agoDespite revenue growth in jewellery sector, natural diamond upstream sees stagnation

-

International News3 hours ago

International News3 hours agoIndia Pavilion at HK twin shows showcases exceptional craftsmanship

-

International News3 hours ago

International News3 hours agoGold continues to get strength on the Middle East conflict

-

National News4 hours ago

National News4 hours agoIJEX 6TH Fam provides comprehensive insights into ME market