International News

Bangkok Gems and Jewelry Fair 2025

Shines Bright, Generating Over 3.7 Billion Baht in Sales

The Department of International Trade Promotion (DITP) and the Gem and Jewelry Institute of Thailand (GIT) have announced the remarkable success of the 71st Bangkok Gems and Jewelry Fair, held from February 22–26, 2025, at the Queen Sirikit National Convention Center. The event exceeded all expectations, drawing nearly 40,000 visitors from across the globe and generating over 3.7 billion baht in trade value. This reinforces Thailand’s position as a global hub for the gem and jewelry industry. With demand surging, organizers are already preparing for the 72nd edition, with exhibition space nearly fully booked.

Sunanta Kangvalkulkij, Director-General of DITP, highlighted the significance of the event: “The Bangkok Gems and Jewelry Fair is a premier international trade show that serves as a key platform for buyers and traders worldwide. Held twice a year, in February and September, the 71st edition saw an expanded exhibition area to accommodate growing industry demand, featuring over 2,628 booths. The response was overwhelmingly positive, with more than 40,000 visitors—71% of whom were international attendees—driving total trade value to 3.718 billion baht, a 3.35% increase from the previous edition. The top five best-selling product categories included gemstones, fine jewelry, silver jewelry, gold and fine jewelry, and diamonds. The fair’s continued success underscores its reputation as a premier global business platform for the gems and jewelry sector.

Her Royal Highness Princess Sirivannavari Nariratana Rajakanya graciously presided over the opening ceremony of the 71st Bangkok Gems and Jewelry Fair on February 22, 2025. In a moment of great honor, Her Royal Highness granted permission to showcase her high jewelry creations in the special exhibition AMOUR ÉTERNEL HAUTE JOAILLERIE. This prestigious display was a highlight of the event, demonstrating the Princess’s commitment to preserving Thai craftsmanship and promoting the Thai jewelry industry on the global stage. The exhibition received an overwhelming response from visitors.”

Sumed Prasongpongchai, Director-General of GIT, emphasized the fair’s role in reinforcing Thailand’s status as a leading gem and jewelry hub: “Bangkok Gems and Jewelry Fair is a must-attend event in the global gem and jewelry industry. It highlights Thailand’s expertise as a center for gemstone enhancement and trading, as well as its world-class artisans known for their exquisite craftsmanship. The fair also offered a range of industry-focused activities, including marketing seminars, technical knowledge-sharing sessions, and the highly anticipated Networking Reception, which brought together key figures from the Thai and international jewelry industries.” The overwhelmingly positive reception from exhibitors and buyers alike has resulted in strong demand for the next edition, with most exhibition booths already reserved. Organizers are confident that the upcoming 72nd edition will be even bigger and more successful.

Save the Date: 72nd Bangkok Gems and Jewelry Fair

The next edition of the Bangkok Gems and Jewelry Fair will take place from September 9–13, 2025, at the Queen Sirikit National Convention Center. Interested exhibitors and visitors can find more information or book exhibition space in advance by contacting +66 2 634 4999 ext. 639 or visiting www.bkkgems.com.

International News

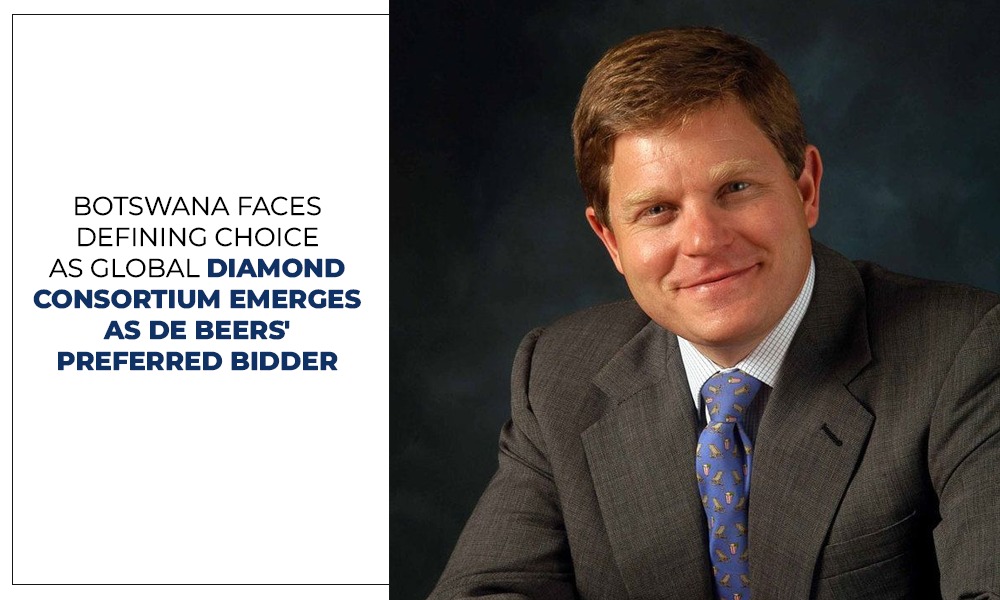

Consortium Led By Former De Beers CEO Gareth Penny Selected As The Preferred Bidder To Acquire De Beers

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers

A consortium headed by former De Beers CEO Gareth Penny has been selected as the preferred bidder to acquire De Beers, according to Botswana’s Minister for State President, Defence and Security, Moeti Mohwasa.

Speaking on the development, Mohwasa said Anglo American conducted a competitive sale process involving three shortlisted bidders before identifying the Global Diamond Consortium as its preferred choice.

Anglo American announced plans to divest De Beers in May 2024 as part of a broader restructuring strategy, driven by prolonged weakness in the diamond market and other business priorities.

The sale process has attracted significant interest from industry leaders and investors. Among those previously linked to the bidding were former De Beers CEO Bruce Cleaver, Australian mining executive Michael O’Keeffe, Indian billionaire Anil Agarwal, and Indian diamond companies KGK Group and Kapu Gems.

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers and retains important rights under the shareholder agreement. Mohwasa emphasized that Botswana has the flexibility to either join the preferred bidder as a strategic partner or exercise its pre-emptive rights independently or with another investor.

Industry observers believe the eventual owner will seek to preserve De Beers’ vertically integrated business model, spanning diamond mining, trading and global natural diamond marketing, while positioning the company to benefit from a potential recovery in natural diamond demand and prices.

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

FIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

BrandBuzz16 hours ago

BrandBuzz16 hours agoFIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

-

National News15 hours ago

National News15 hours agoNature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

-

National News12 hours ago

National News12 hours agoRajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

New Premises14 hours ago

New Premises14 hours agoVinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai