International News

WGC Gold Market Commentary: Strong euro and tariff fears drive gold

Another month, another set of new highs. Gold finished March 2025 at US$3,115/oz, a gain of 9.9% m/m.Even a materially weaker US dollar, primarily via euro strength, couldn’t prevent a stellar performance and new highs across all other major currencies .

According to our Gold Return Attribution Model (GRAM), euro strength and thus US dollar weakness was once again a key driver of gold’s performance, alongside an increase in geopolitical risk capturing tariff fears. Gold ETF buying continued apace in March with all regions contributing. US funds led the charge with US$6bn (67t) of net inflows followed by Europe then Asia with approximately US$1bn each. While ETF flows were positive, COMEX futures declined marginally by US$400mn (5t) likely on profit taking.

March review

A stronger euro, tariff fears and ETF buying edged gold to new highs once again in March.

Looking forward

Fiscal and monetary support may be receding, and the timing isn’t great for risk assets given current turmoil. Fundamentals remain solid for gold.

• Liquidity matters, and has arguably been bolstering both financial assets and the economy in the US for much of the post-COVID period

• In 2022, however, US financial conditions tightened forcefully as liquidity was removed from markets. This perfect storm caused a very rare annual joint decline in bonds and equities. Gold held up but also experienced some bumps along the way

• We are now at a similar impasse in liquidity conditions, but with crucial differences that bode well fundamentally for gold

• The one hurdle is the hitherto strong run-up in gold prices. Comparisons to the 2011 and 2020 peaks are likely to be made, but in our view, the environment remains supportive of further gains.

While by no means the sole contributors to their solid performance, the US economy and financial markets benefited from monetary and fiscal support since the COVID pandemic.

activity). Gold also succumbed, falling 20% over two quarters

in 2022, before a recovery to end the year flat. Proving direct causality is difficult, yet it does suggest markets and the economy had grown accustomed to artificial support.

At a crossroads

While much of the conversation over the past week has centred around tariffs, liquidity risk remains an important undercurrent. And we believe we may now be approaching a similar impasse to what markets experienced in 2022.

Quantitative tightening is slowing but there has been no mention of a resumption of quantitative easing. Indeed, the appetite might not be there given the high levels of debt and sticky inflation. In addition, constraints on government spending via the Department of Government Efficiency (DOGE) are stifling fiscal support. And the Fed’s Overnight Reverse Repo facility (ON RRP) is low, which provides less wiggle room for the Fed to manage liquidity issues. This appears to be showing up in stats like order-book liquidity for equity futures and – as flagged in the Fed’s financial stability report in November– on-the-run bond liquidity. It may also be contributing to the year-to-date equity rout.

And the labour market is flirting with contraction as hours worked are in steep decline. Logically they lead an employment slowdown as companies reduce hours for staff before layoffs; statistically this also appears to be the case. But layoffs are also now on the rise and are likely to feed into payroll numbers in due course (Chart 5). To add to this, uncertainty surrounding tariffs has supercharged concerns about the resiliency of labour markets in the short and medium term.

While inflation was rising more in 2022, it was driven by growth. This time around inflation is sticky while growth is faltering, resulting in a stagflationary environment. In this context, rates are unlikely to be going up from here and further weakening of the dollar is likely on waning US exceptionalism

Central banks have been strong contributors to gold’s performance over the past three years and show few signs of letting up, adding fundamental support to prices

US gold ETF investors had built up sizeable holdings in 2020 prior to the 2022 wobbles. But they have been sidelined until recently, suggesting capacity to keep adding.

Fundamentals remain in place…

The current run-up in price has taken many by surprise. Paraphrasing an old adage, shouldn’t high prices for a commodity cure high prices? Gold is not a commodity in the traditional sense and primary production’s response may have only limited impact on price. The willingness to hold and reluctance to sell – given current extreme policy uncertainty – could generate real momentum. By historical standards, the current rally isn’t particularly large or long. And comparing the current rally to the recent 2011 and 2020 peaks highlights that, relatively speaking, fundamentals look more solid (Table 2):

• US gold ETFs are a considerably smaller share of all US ETF assets than during 2011 as ETF buyers have been on the sidelines for the best part of four years they are not overbought

• Real yields are higher and above their long-run average, suggesting more downside than upside risk for yields – and vice versa for gold prices

• Forward equity price-to-earnings remains high, and that provides capacity for further downside to equities should an economic slowdown and earnings downgrades worsen, especially in the current geoeconomic conditions, a boon for gold’s safe-haven appeal

• Credit spreads are considerably tighter than during the two previous peaks. Again, widening risks trump contraction risk, and are also gold supportive.

• The dollar remains elevated relative to prior periods even if it has weakened since the start of the year. With the Trump administration favouring a weaker dollar and the uncertain effect of tariffs, this could serve as an additional tailwind for gold.

…But not without risks

But we also caution that there are risks for the gold price after a rally such as this in such a short space of time.

Treasury managers at central banks could prudently slow their pace of buying given the price rally, as we saw with some central banks last year. While consumer demand adapts to higher prices eventually, the speed of price moves is like to dampen net buying in the near term. A liquidity crunch could negatively affect gold as the most liquid assets are sold to meet margin calls.

Additionally, geopolitical and policy nervousness is quite elevated, particularly given significant uncertainty about tariffs and its effect on market volatility, which is likely adding a meaningful premium to gold prices. Any resolution could bring that premium out as we have seen in previous historical periods.

In sum…

The extent and speed of gold’s rally has drawn out comparisons to previous peaks. While there are headwinds that the gold market will naturally face in this environment, our analysis also suggest that current macroeconomic conditions are quite different to prior periods when the gold market reached previous highs.

International News

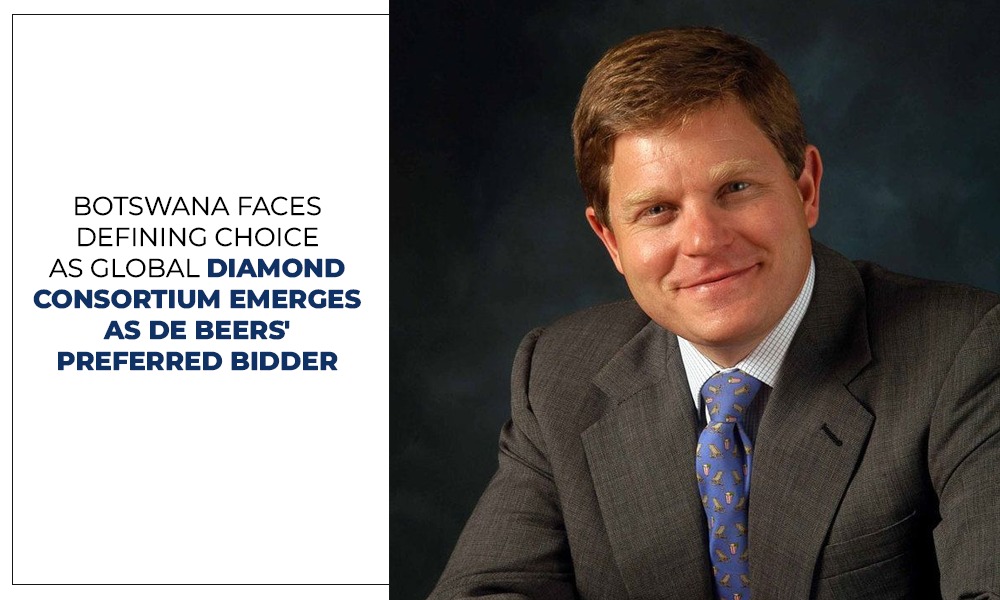

Consortium Led By Former De Beers CEO Gareth Penny Selected As The Preferred Bidder To Acquire De Beers

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers

A consortium headed by former De Beers CEO Gareth Penny has been selected as the preferred bidder to acquire De Beers, according to Botswana’s Minister for State President, Defence and Security, Moeti Mohwasa.

Speaking on the development, Mohwasa said Anglo American conducted a competitive sale process involving three shortlisted bidders before identifying the Global Diamond Consortium as its preferred choice.

Anglo American announced plans to divest De Beers in May 2024 as part of a broader restructuring strategy, driven by prolonged weakness in the diamond market and other business priorities.

The sale process has attracted significant interest from industry leaders and investors. Among those previously linked to the bidding were former De Beers CEO Bruce Cleaver, Australian mining executive Michael O’Keeffe, Indian billionaire Anil Agarwal, and Indian diamond companies KGK Group and Kapu Gems.

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers and retains important rights under the shareholder agreement. Mohwasa emphasized that Botswana has the flexibility to either join the preferred bidder as a strategic partner or exercise its pre-emptive rights independently or with another investor.

Industry observers believe the eventual owner will seek to preserve De Beers’ vertically integrated business model, spanning diamond mining, trading and global natural diamond marketing, while positioning the company to benefit from a potential recovery in natural diamond demand and prices.

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

FIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

BrandBuzz10 hours ago

BrandBuzz10 hours agoFIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

-

National News9 hours ago

National News9 hours agoNature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

-

National News6 hours ago

National News6 hours agoRajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

National News10 hours ago

National News10 hours agoMCX Gold, Silver Futures Surge