International News

WGC 2024 Central Bank Gold Reserves Survey

Central Bank managers will continue to increase their gold holdings in the next 12 months

Central Bank managers will continue to increase their gold holdings in the next 12 months

An increasingly complex geopolitical and financial environment is making gold reserves management more relevant than ever. In 2023, central banks added 1,037 tonnes of gold – the second highest annual purchase in history – following a record high of 1,082 tonnes in 2022.

Following these record numbers, gold continues to be viewed favourably by central banks as a reserve asset. According to the 2024 Central Bank Gold Reserves (CBGR) survey, which was conducted between 19 February and 30 April 2024 with a total of 70 responses, 29% of central banks respondents intend to increase their gold reserves in the next twelve months, the highest level we have observed since we began this survey in 2018.

The planned purchases are chiefly motivated by a desire to rebalance to a more preferred strategic level of gold holdings, domestic gold production, and financial market concerns including higher crisis risks and rising inflation.

81 per cent said that official sector gold reserves overall will grow in the same period. Optimism towards gold’s future role in global reserves continues to grow, with 69% saying that gold’s share of reserves will be higher in five years compared to 62% last year, the WGC survey said.

The top reasons given for the increases now are “long-term store of value or inflation hedge,” “performance during times of crisis” and “effective portfolio diversifier.”

According to the report, reserve managers indicate that they are looking to gold to help mitigate risks and prepare for further political and economic uncertainty, globally. Although seven in ten (71%) still view gold’s legacy as a reason to hold it, other reasons have surpassed it this year. The top three reasons to hold gold now include: gold’s long-term value (88%), performance during crisis (82%), and its role as an effective portfolio diversifier (76%).

Central banks in emerging markets and developing economies (EMDE) maintained their positive outlook for gold’s future share in reserves portfolios. Notably, they were joined by advanced economy central banks which now view gold more positively. More than half (57%) of this group said gold would account for a higher proportion of reserves five years from now, a significant increase compared to 2023 (when 38% of respondents indicated the same view).

Advanced economy central banks have also become more pessimistic in their outlook for the US dollar’s share of global reserves, a view which has consistently been more prominent among EMDEs. More than half (56%) of advanced economy respondents believe the US dollar’s share of global reserves will fall (up 10 percentage points year-on-year), while 64% of EMDE respondents share the same view.

Demand for gold from central banks has been elevated in the last two years as some countries diversify their foreign currency reserves. Their demand contributed to the gold price rally in March-May with the spot price hitting a record high of $2,449.89 per ounce on May 20.

International News

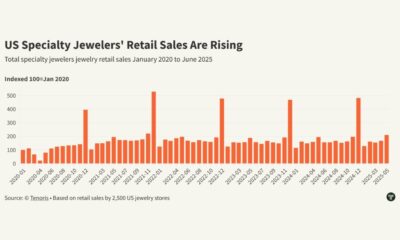

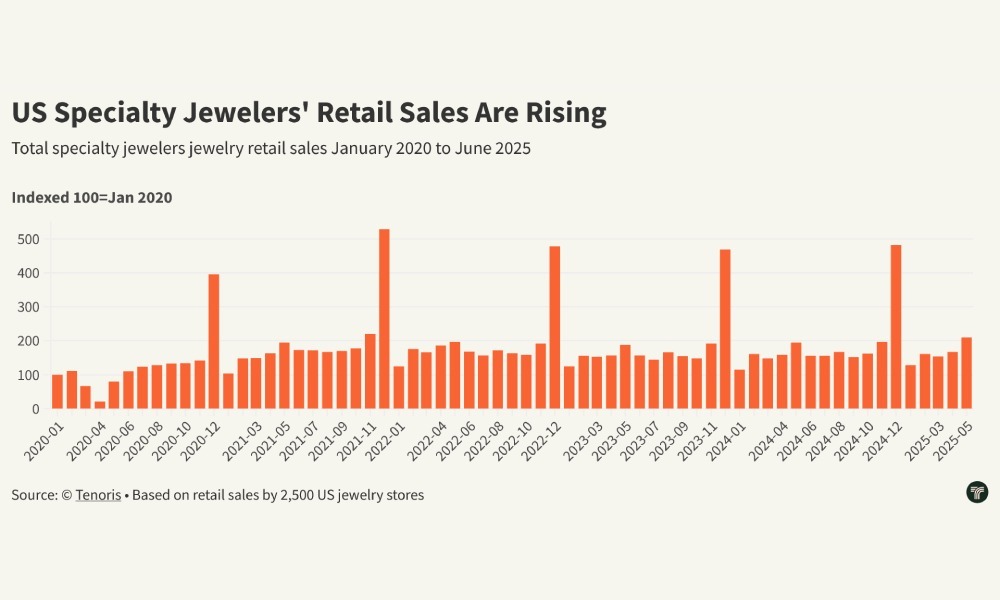

Tenoris Report: 5% rise in jewellery sales in H1 2025

Gold jewellery led category growth with low double-digit revenue gains

The jewellery market posted a healthy 5% revenue growth in H1 2025, according to Tenoris, sustained by a steady five-month rise and a 3% increase in June sales. While the total number of pieces sold declined, consumers spent more per item, leading to a 10% surge in expenditure per unit in June and higher average prices across diamond, sapphire, gold, platinum, and silver jewellery.

Lab-grown jewels stood out, recording higher unit sales despite falling average prices, reflecting shifting consumer preferences. Round diamonds, though still dominant at 52% of sales, are gradually losing ground to oval shapes, which now account for 20%.

Finished jewellery also performed well, especially bracelets, which saw nearly 10% year-on-year revenue growth. Demand is strengthening in higher price segments, notably items priced between $7,500 and $10,000.

Natural diamond jewellery sales dipped in June but rose 3% year-to-date, driven by demand for pendants, bracelets, and necklaces above $2,500, often featuring lab-grown diamonds. The loose natural diamond market saw higher average carat weights but longer inventory turnover, while lab-grown loose diamonds continued to capture market share. Overall, the industry is rebounding from flat sales in H1 2024 and is focused on tapping new consumer demographics to sustain momentum.

International News

Gold edges lower on rebounding Dollar as trade war intensifies AUGMONT BULLION REPORT

As the trade war heats up, the dollar trades at a two-week high against the yen, while gold drops below $3300.

- A 50% tariff on copper imports, possible 200% duties on pharmaceuticals, and a 10% levy on goods from BRICS nations are just a few of the extensive new measures that President Donald Trump announced, ruling out future extensions to the August 1 tariffs.

- Meanwhile, following a strong US jobs report last week, which allayed concerns about a slowing economy, the Fed lowered its July rate drop predictions.

- The expectation for more rate cuts has also decreased because the tariffs are anticipated to increase US inflation in the upcoming months.

- Investors are now waiting for the minutes of the June FOMC meeting to be released in order to gain further understanding of the Fed’s policy position.

Technical Triggers

- Gold continues to trade near the lower side of the range of $3300 (~Rs 96250) and $3400 (~Rs 98500). If prices sustain below $3280 (~Rs 96000), weakness could further extend to $3200 (~Rs 94000).

- Silver is not able to sustain above its range of $37.5 (~ Rs 108,500) and $35.5 (~ Rs 105,000). Consolidation continues before heading higher towards the next target is $38 (~Rs 110,000)

Support and Resistance

For Gold

| Region | Support Level | Resistance Level |

|---|---|---|

| International Gold | $3280/oz | $3370/oz |

| Indian Gold | ₹96,000/10 gm | ₹97,700/10 gm |

For Silver

| Region | Support Level | Resistance Level |

|---|---|---|

| International Silver | $35.5/oz | $37.5/oz |

| Indian Silver | ₹1,05,000/kg | ₹1,10,000/kg |

International News

WGC REPORT :Gold ETF Flows- June 2025

Global gold ETFs’ total AUM rose to a month-end peak and holdings bounced to the highest in 34 months

H1 in review

Global physically backed gold ETFs1 saw inflows of US$38bn during H1, boosted by strong positive flows in June (Chart 1), marking the strongest semi-annual performance since H1 2020.2 All regions saw inflows last month, with North American and European investors leading the charge.

During the first half, North America accounted for the bulk of inflows, recording the strongest H1 in five years. And despite slowing momentum in May and June, Asian investors bought a record amount of gold ETFs during H1, contributing an impressive 28% to net global flows with only 9% of the world’s total assets under management (AUM). European flows finally turned positive in H1 2025 following non-stop semi-annual losses since H2 2022.

By the end of H1 the surging gold price and notable inflows pushed global gold ETFs’ total AUM 41% higher to US$383bn, a month-end record. Collective holdings in H1 grew 397t to 3,616t, the highest month-end value since August 2022 (Chart 2).

Regional overview

North America attracted US$4.8bn in June – the strongest monthly inflow since March – bringing total H1 inflows to US$21bn. Spiking geopolitical risks amid the Israel-Iran conflict boosted investor demand for safe-haven assets and supported inflows into North American gold ETFs. Although it held rates steady in June, the US Fed continued to express concerns about slowing growth and rising inflation.3 Markets are now pricing in three rate cuts by the end of 2025 and an additional two in 2026.

The investor response has been swift: US Treasury yields declined, and the dollar continued to weaken. Persistent policy uncertainty and ongoing fiscal concerns are likely to remain an overhang on the market, which in turn could help support gold ETF demand in the near to medium term.

European inflows continued for a second month, adding US$2bn in June – the strongest since January – and lifting the region’s H1 total to US$6bn. The UK led inflows in the month; although the Bank of England kept rates unchanged at its June meeting, the stance was generally dovish. 4 Combined with weaker growth, easing inflation and the cooling labour market, investors raised their bets on future rate cuts. This resulted in local yields declining and pushed up gold’s allure. Meanwhile, the eighth cut from the European Central Bank, uncertainties surrounding growth, and rising geopolitical risks generally, contributed to gold ETF demand in several major markets.

Asian flows flipped positive in June, albeit only mildly at US$610mn, ending at US$11bn – a record amount for any H1 period. India led inflows in June, likely supported by rising geopolitical risks in the Middle East. Japan recorded inflows for the ninth consecutive month (US$198mn, US$1bn H1), possibly driven by elevated inflationary concerns – particularly when the rice price surged.6 China only saw mild inflows in the month (US$137mn) as trade tensions eased and the local gold price moderated.7 Nonetheless, China’s H1 inflows of US$8.8bn (85t) were unprecedented amid spiking trade risks with the US, growth concerns and the surging gold price.

ALROSA’s Severalmaz ramps up output as Karpinsky-2 diamond pipe enters development

PC Jeweller Soars 33% in Two Days on Strong Q1 Revenue Growth and Debt Reduction Plans

Senco Gold Q1 Revenue Jumps 28% on Festive Demand and Store Expansion

ALROSA’s Severalmaz ramps up output as Karpinsky-2 diamond pipe enters development

PC Jeweller Soars 33% in Two Days on Strong Q1 Revenue Growth and Debt Reduction Plans

Senco Gold Q1 Revenue Jumps 28% on Festive Demand and Store Expansion

-

National News5 days ago

National News5 days agoMalabar Gold & Diamonds Inaugurates Landmark Integrated Manufacturing Site in Hyderabad, Cementing Its Position as a Global Manufacturing Leader

-

National News2 months ago

National News2 months agoEmmadi Silver Jewellery Launches First Karnataka Store with Grand Opening in Bengaluru’s Malleshwaram

-

BrandBuzz3 months ago

BrandBuzz3 months agoMia by Tanishq Unveils ‘Fiora’ Collection This Akshaya Tritiya: A Celebration of Nature’s Blossoms and New Beginnings

-

GlamBuzz2 months ago

GlamBuzz2 months agoGokulam Signature Jewels Debuts in Hyderabad with Glamorous Launch at KPHB