International News

Titan in Talks to Buy Stake in Damas Jewellery for Rs 4,500 Cr

The acquisition could boost Titan’s presence in the GCC’s luxury jewellery market.

Titan Co., the Tata Group’s watch and jewellery arm, is in discussions with Qatar-based Mannai Corp to acquire a significant stake in Damas Jewellery, a leading retailer in South Asia, for Rs 4,500 crore, according to The Economic Times. While talks are ongoing, no agreement has been finalized.

This marks Titan’s second attempt to strike a deal with Damas after previous negotiations stalled over valuation concerns. The renewed discussions highlight Titan’s strategy to expand in the Gulf Cooperation Council (GCC) region, a key market for its international growth.

Valuation is contingent on Damas’ business structure and bullion stock, with a higher stock potentially increasing the valuation, according to an industry analyst.

Mannai Corp, which fully acquired Damas in April 2012, owns the company. Headquartered in Dubai, Damas is a prominent jewellery retailer in the GCC.

Titan’s jewellery brand Tanishq has been expanding its footprint in the GCC, opening a flagship store in Dubai’s Gold Souk in January and introducing Arabic-inspired collections in stores across the UAE and Qatar.

Titan’s jewellery division, which includes Tanishq, Zoya, CaratLane, and Mia by Tanishq, reported a 20% growth in income for FY24, reaching Rs 38,353 crore. Titan, valued at Rs 58,447 crore, operates across multiple sectors, including wearables, fragrances, fashion accessories, and Indian apparel.

Founded in 1907, Damas operates 300 stores across the GCC and employs over 2,000 people. The company carries luxury brands such as Graff, Djula, Roberto Coin, and Mikimoto alongside its own collections.

Acquiring Damas would strengthen Tanishq’s presence in the GCC market, aligning with Titan’s international expansion goals and providing access to established luxury markets. The UAE, where Damas is based, ranks as the world’s fifth-largest gold jewellery market and has the second-highest per capita gold jewellery consumption globally, after Hong Kong.

International News

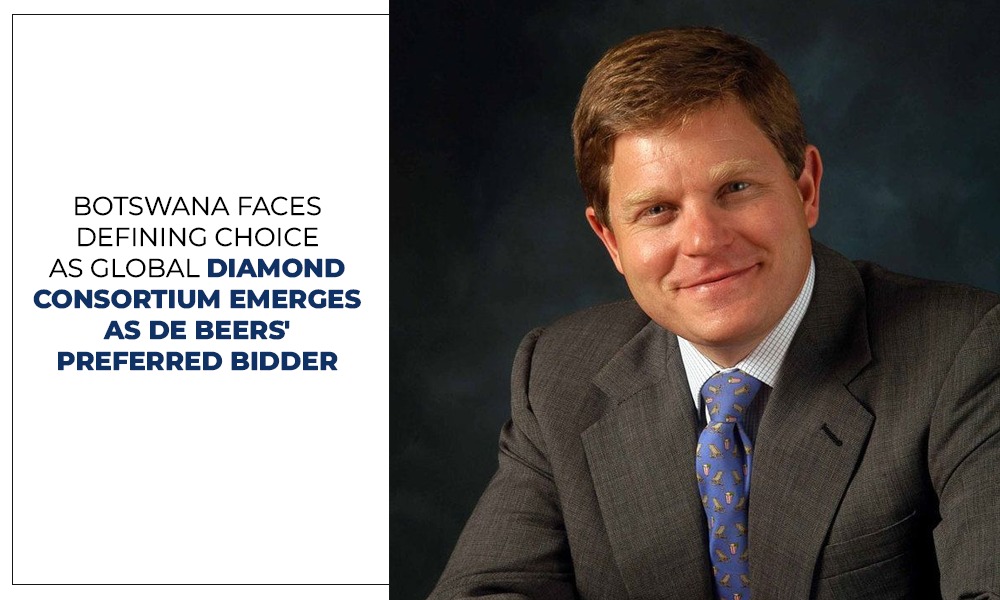

Consortium Led By Former De Beers CEO Gareth Penny Selected As The Preferred Bidder To Acquire De Beers

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers

A consortium headed by former De Beers CEO Gareth Penny has been selected as the preferred bidder to acquire De Beers, according to Botswana’s Minister for State President, Defence and Security, Moeti Mohwasa.

Speaking on the development, Mohwasa said Anglo American conducted a competitive sale process involving three shortlisted bidders before identifying the Global Diamond Consortium as its preferred choice.

Anglo American announced plans to divest De Beers in May 2024 as part of a broader restructuring strategy, driven by prolonged weakness in the diamond market and other business priorities.

The sale process has attracted significant interest from industry leaders and investors. Among those previously linked to the bidding were former De Beers CEO Bruce Cleaver, Australian mining executive Michael O’Keeffe, Indian billionaire Anil Agarwal, and Indian diamond companies KGK Group and Kapu Gems.

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers and retains important rights under the shareholder agreement. Mohwasa emphasized that Botswana has the flexibility to either join the preferred bidder as a strategic partner or exercise its pre-emptive rights independently or with another investor.

Industry observers believe the eventual owner will seek to preserve De Beers’ vertically integrated business model, spanning diamond mining, trading and global natural diamond marketing, while positioning the company to benefit from a potential recovery in natural diamond demand and prices.

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

FIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

BrandBuzz9 hours ago

BrandBuzz9 hours agoFIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

-

National News8 hours ago

National News8 hours agoNature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

-

National News5 hours ago

National News5 hours agoRajiv Jain Elected Chairman Of Jaipur Jewellery Show

-

National News10 hours ago

National News10 hours agoMCX Gold, Silver Futures Surge