International News

Russia and Belarus strengthen alliance to boost jewellery exports amid sanctions

In a strategic move to counter the economic impact of ongoing G7 sanctions, Russia and Belarus have announced a new collaborative effort aimed at promoting jewelry exports to non-Western markets, particularly China, the UAE, Vietnam, and other Southeast Asian nations.

The agreement was formalized following a high-level meeting between Russia’s Deputy Finance Minister, Alexei Moiseyev, and Belarus’s Finance Minister, Yury Seliverstov, held in Minsk, the capital of Belarus. The initiative reflects a broader effort by both countries to pivot eastward, seeking new avenues of trade and economic cooperation outside the Western sphere.

Key Objectives of the Alliance:

- The primary focus of the collaboration is to significantly increase the export of jewelry crafted in Russia and Belarus to emerging and receptive markets in Asia and the Middle East.

- Both ministers discussed strategies to enhance e-commerce capabilities, aiming to make jewelry products more accessible to foreign consumers through digital platforms. The move is seen as essential to overcoming physical trade barriers and reaching wider global audiences.

- Another critical area of cooperation is the mutual recognition of state hallmark standards between Russia and Belarus. This will facilitate smoother cross-border trade, reduce administrative bottlenecks, and present a unified standard of quality to international buyers.

- According to BelTA, Belarus’s state news agency, Deputy Minister Moiseyev announced plans to launch a joint digital marketplace for Russian and Belarusian jewelry by the end of the year. The platform will debut in a test mode, serving as a centralized hub for international consumers and wholesale buyers.

- The initiative is receiving backing from the Eurasian Development Bank (EDB) — a multilateral financial institution co-founded by Russia and Kazakhstan. The EDB’s involvement underscores the strategic importance of the project and is expected to provide essential financial infrastructure and investment support.

- The collaboration emerges against the backdrop of intensifying Western sanctions imposed in response to Russia’s ongoing war in Ukraine, which Belarus has publicly supported. Both countries have been progressively cut off from Western markets and financial systems, compelling them to seek alternative trade routes and alliances.

By focusing on high-value, non-sanctioned commodities such as jewelry, Russia and Belarus are looking to tap into the luxury consumption boom in Asia and the Gulf region. These markets are seen as more neutral or supportive of Moscow and Minsk’s geopolitical positions and are increasingly receptive to alternative sources of luxury goods.

The move signals a broader shift in trade strategy for both nations, away from reliance on traditional Western markets and towards building resilient economic partnerships within the Eurasian, Asian, and MENA regions. If successful, this jewelry export initiative could serve as a template for other sectors seeking to navigate the constraints of international sanctions.

Moiseyev emphasized that this collaboration was just the beginning of deeper economic integration and joint trade development between Russia and Belarus. With the launch of the e-commerce platform and increased outreach to Asia and the Middle East, the two nations are positioning themselves to not only preserve their industries under sanctions but also thrive in new markets.

International News

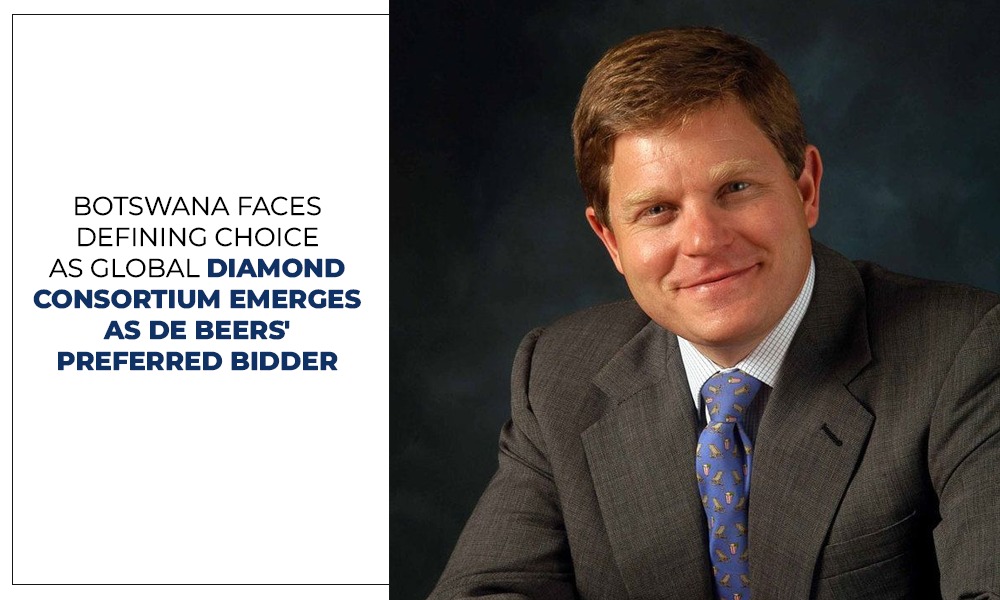

Consortium Led By Former De Beers CEO Gareth Penny Selected As The Preferred Bidder To Acquire De Beers

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers

A consortium headed by former De Beers CEO Gareth Penny has been selected as the preferred bidder to acquire De Beers, according to Botswana’s Minister for State President, Defence and Security, Moeti Mohwasa.

Speaking on the development, Mohwasa said Anglo American conducted a competitive sale process involving three shortlisted bidders before identifying the Global Diamond Consortium as its preferred choice.

Anglo American announced plans to divest De Beers in May 2024 as part of a broader restructuring strategy, driven by prolonged weakness in the diamond market and other business priorities.

The sale process has attracted significant interest from industry leaders and investors. Among those previously linked to the bidding were former De Beers CEO Bruce Cleaver, Australian mining executive Michael O’Keeffe, Indian billionaire Anil Agarwal, and Indian diamond companies KGK Group and Kapu Gems.

Botswana is expected to play a pivotal role in the transaction. The country, together with Namibia, Angola and other shareholders, already owns a 15% stake in De Beers and retains important rights under the shareholder agreement. Mohwasa emphasized that Botswana has the flexibility to either join the preferred bidder as a strategic partner or exercise its pre-emptive rights independently or with another investor.

Industry observers believe the eventual owner will seek to preserve De Beers’ vertically integrated business model, spanning diamond mining, trading and global natural diamond marketing, while positioning the company to benefit from a potential recovery in natural diamond demand and prices.

Bollywood Star Rakul Preet Singh Unveils Senco Gold & Diamonds’ Flagship Store in Bhubaneswar

Rajiv Jain Elected Chairman Of Jaipur Jewellery Show

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

Bollywood Star Rakul Preet Singh Unveils Senco Gold & Diamonds’ Flagship Store in Bhubaneswar

Nature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

Vinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai

-

New Premises50 minutes ago

New Premises50 minutes agoBollywood Star Rakul Preet Singh Unveils Senco Gold & Diamonds’ Flagship Store in Bhubaneswar

-

BrandBuzz22 hours ago

BrandBuzz22 hours agoFIFA Unveils First-Ever 18K Gold Diamond Championship Rings to celebrate Spain’s World Cup Victory

-

National News21 hours ago

National News21 hours agoNature’s Elegance, Reimagined: Lotus Arts De Vivre’s Cape Gooseberry Earrings Continue To Captivate

-

New Premises20 hours ago

New Premises20 hours agoVinsmera Jewels Expands UAE Presence With Soft Opening Of New Al Barsha Showroom In Dubai