International News

Hard Pure Gold to redefine China gold jewellery sector

Record-high gold prices and continued geopolitical uncertainty have strengthened gold’s appeal as a safe-haven asset. However, these same factors also create challenges for the jewellery industry, as rising prices increase the cost of entry for consumers. In response, the industry is exploring product innovation to sustain demand. In Greater China, Hard Pure Gold is emerging as a strategic initiative designed to balance high purity, design flexibility, and affordability.

Promoted by the World Gold Council, Hard Pure Gold combines traditional purity levels—typically above 99%—with advanced manufacturing technologies such as electroforming and lost-wax casting. These processes increase the hardness of pure gold, allowing jewellers to create more intricate designs, improve durability, and support gemstone settings. At the same time, hollow-forming techniques enable lighter pieces that maintain visual impact while reducing overall weight and price.

The category also benefits from the introduction of an industry-wide standard in 2025, which clarified production guidelines and unified marketing terminology across manufacturers. Standardisation has helped build consumer trust and strengthened the positioning of Hard Pure Gold as a distinct product segment.

A key driver of its growth is changing consumer demographics. Traditionally, pure gold jewellery in China appealed primarily to middle-aged buyers who valued gold for wealth preservation. Hard Pure Gold, however, is attracting younger consumers aged 20–35 by offering contemporary designs, lighter weight, and lower entry prices without sacrificing purity. Surveys conducted by the World Gold Council indicate that it is currently the fastest-growing category within the gold jewellery segment in Greater China.

In a high-price environment, the ability to produce jewellery that looks substantial yet weighs as little as 1.5 grams helps make gold more accessible to new buyers. At the same time, increasing trade-in activity—where consumers exchange older jewellery for newer designs—encourages repeat purchases and keeps demand active.

From a strategic perspective, Hard Pure Gold demonstrates how technological innovation and coordinated industry standards can reshape consumer perception. By merging investment-grade purity with modern design and affordability, it offers a compelling pathway for sustaining gold jewellery demand in Greater China

International News

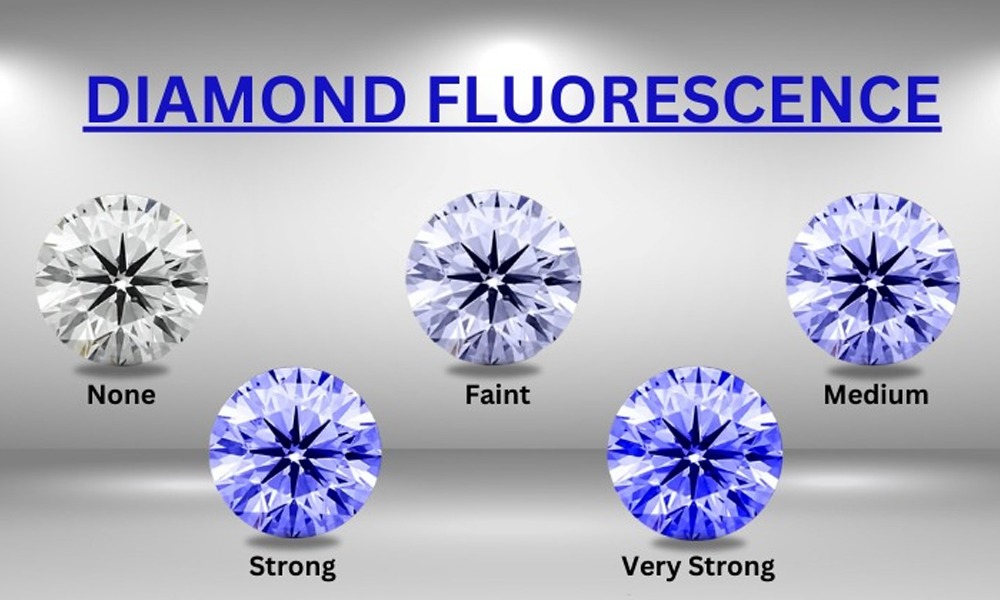

Fluorescent Diamonds: GIA to Introduce Clearer Guidance

According to GIA, around 25% to 35% of all diamonds show some level of fluorescence. Greater transparency about this significant segment of the market could help improve confidence among both consumers and the jewellery trade.

Later this year, the Gemological Institute of America (GIA) will introduce new wording in its diamond grading reports to reduce confusion about fluorescent diamonds. The update, expected in the fourth quarter, is one of the most important steps taken by a grading laboratory to explain this feature more clearly to both the jewellery trade and consumers.

Rapaport Intelligence Report explores what this change could mean for the diamond market. Fluorescence has had a long and complicated history. In the past, fluorescent diamonds often sold at premium prices. However, attitudes changed during the diamond boom of the 1970s and again after a grading controversy in South Korea in the early 1990s. Although later gemological research helped improve confidence in fluorescent diamonds, many buyers still view them negatively, and they often sell at discounted prices.

The report also looks at how these discounts have changed over the past six years through both strong and weak market conditions. In addition, the report explains two key questions: how fluorescence affects a diamond’s appearance and whether it influences its color grade. It also considers whether GIA’s new report comments could change how buyers view fluorescent diamonds.

The report revisits a long-debated issue—does fluorescence really affect a diamond’s beauty, or are today’s concerns mainly based on old perceptions that continue to influence buying decisions?

According to GIA, around 25% to 35% of all diamonds show some level of fluorescence. Greater transparency about this significant segment of the market could help improve confidence among both consumers and the jewellery trade.

The Rise Of Everyday Milestone Gifting:Why Natural Diamond Solitaires Are No Longer Reserved For Weddings

Style, Silver & Scale: How Kushals Is Redefining India’s Fashion Jewellery Landscape

P N Gadgil Jewellers Delivers Record Q1 FY27 Revenue Of 24,130 Mn; With 41% Revenue Growth, 57% EBITDA Growth & 52% PAT Growth; YoY

P N Gadgil & Sons Opens New Showroom At Amanora Mall, Hadapsar, Pune

Style, Silver & Scale: How Kushals Is Redefining India’s Fashion Jewellery Landscape

P N Gadgil Jewellers Delivers Record Q1 FY27 Revenue Of 24,130 Mn; With 41% Revenue Growth, 57% EBITDA Growth & 52% PAT Growth; YoY

-

New Premises4 hours ago

New Premises4 hours agoP N Gadgil & Sons Opens New Showroom At Amanora Mall, Hadapsar, Pune

-

JB Insights33 minutes ago

JB Insights33 minutes agoStyle, Silver & Scale: How Kushals Is Redefining India’s Fashion Jewellery Landscape

-

By Invitation17 minutes ago

By Invitation17 minutes agoThe Rise Of Everyday Milestone Gifting:Why Natural Diamond Solitaires Are No Longer Reserved For Weddings

-

National News1 hour ago

National News1 hour agoP N Gadgil Jewellers Delivers Record Q1 FY27 Revenue Of 24,130 Mn; With 41% Revenue Growth, 57% EBITDA Growth & 52% PAT Growth; YoY