National News

GJEPC addresses issue of Termination of IEEPA-Based Reciprocal Tariffs

GJEPC informed all exporter members of an important interim development concerning U.S. import duties applicable to Indian exports, particularly in the gem and jewellery sector.

The Gem & Jewellery Export Promotion Council (GJEPC) informed all exporter members of an important interim development concerning U.S. import duties applicable to Indian exports, particularly in the gem and jewellery sector.

A letter issued by Sabyasachi Ray, Executive Director, GJEPC, addressed the Termination of IEEPA-Based Reciprocal Tariffs and outlined key implications for exporters.

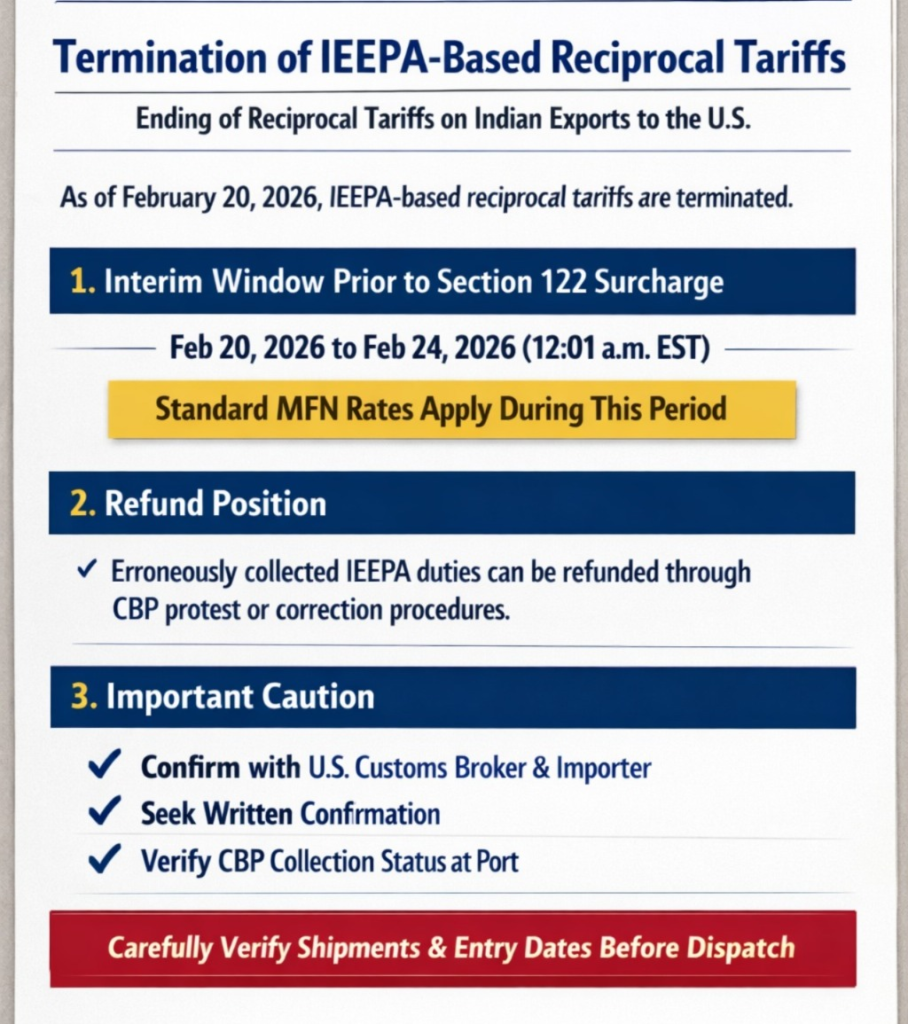

Termination of IEEPA-Based Reciprocal Tariffs

Pursuant to the Executive Order dated February 20, 2026, titled “Ending Certain Tariff Actions”, the additional ad valorem duties imposed under IEEPA, including the reciprocal tariff framework under Executive Order 14257, shall no longer remain in effect and are directed to be terminated as soon as practicable.

Accordingly, entries made on or after February 20, 2026 should not be subject to the earlier IEEPA-based reciprocal tariffs.

1. Interim Window Prior to Section 122 Surcharge

A separate Presidential Proclamation dated February 20, 2026 imposes a temporary 10% surcharge under Section 122 of the Trade Act of 1974, effective 12:01 a.m. EST on February 24, 2026.

Therefore, between: February 20, 2026 – before 12:01 a.m. EST on February 24, 2026 imports into the United States should be subject only to ordinarily applicable HTSUS (MFN) rates, without the earlier reciprocal tariff, and prior to the commencement of the Section 122 surcharge.

For products such as cut and polished diamonds (where the MFN rate is ordinarily 0%), this period represents a limited operational window.

2. Refund Position (If Collected in Error or Due to Implementation Lag)

In cases where reciprocal IEEPA duties are collected due to implementation lag, such duties should be eligible for refund through the standard:

- U.S. Customs and Border Protection (CBP) protest mechanism under 19 U.S.C. §1514, or

- Post-summary correction procedures, as applicable.

However, exporters should note that there is no assurance that the refund process will not be time-consuming.

3. Important Caution for Exporters

While GJEPC is actively engaging with U.S. customs authorities and keeping customs at Bharat Diamond Bourse informed, members are strongly advised to:

- Seek confirmation from their U.S. customs broker and trade counsel

- Obtain written confirmation from their U.S. buyer/importer regarding entry treatment

- Confirm that CBP has ceased collection of the reciprocal tariff at the port of entry

Given the evolving implementation environment, entry-level verification is critical.

Members are encouraged to carefully assess:

- Shipment timing

- Entry dates

- Applicable HTS classification

before dispatching consignments, wherever applicable.

source: GJEPC

National News

Palmonas Raises $40 Million in Series B, Accelerates Omni-Channel Expansion

Shraddha Kapoor-Backed Demi-Fine Jewellery Brand to Scale Offline Retail and Strengthen Market Presence

Palmonas, the Shraddha Kapoor-backed demi-fine jewellery startup, has raised $40 million (approx. Rs. 373 crore) in a Series B funding round, led by Xponentia Capital and Vertex Growth Fund, with participation from existing investor Vertex Venture

The fresh capital will be utilised to expand its offline retail footprint, building on its growing omnichannel presence across online platforms and physical stores.

Founded in 2022 by Pallavi Mohadikar and Amol Patwari, with Shraddha Kapoor joining as co-founder, Palmonas operates in the demi-fine jewellery segment, offering affordable yet premium designs crafted from sterling silver and stainless steel with gold plating. The brand targets the space between fashion and fine jewellery, catering to a young, aspirational audience.

The company has seen rapid growth, with its operating revenue surging over 40X to Rs. 39 crore in FY25, up from Rs. 97 lakh in FY24. Notably, Palmonas also turned profitable, reporting a profit of Rs. 4.3 crore during the same period.

The brand had earlier raised Rs. 55 crore from Vertex Ventures and gained visibility through Shark Tank India Season 4, securing Rs. 1.26 crore funding from Namita Thapar and Ritesh Agarwal, at a Rs. 126 crore valuation.

Operating in a competitive space, Palmonas goes head-to-head with players such as GIVA, BlueStone, and Limelight Lab Grown Diamonds, as it continues to strengthen its position in India’s fast-growing demi-fine jewellery market.

Triptii Dimri Launches Hues By Tanishq; Collection Showcases The Vibrant Colours Of Natural Gemstones

Botswana Stepping Up Diplomatic Efforts To Complete The Removal Of US Tariffs

P. N. Gadgil & Sons Expands in Pune with New Store at Tribeca Highstreet; Launches 9KT Collection

P. N. Gadgil & Sons Expands in Pune with New Store at Tribeca Highstreet; Launches 9KT Collection

Palmonas Raises $40 Million in Series B, Accelerates Omni-Channel Expansion

Botswana Stepping Up Diplomatic Efforts To Complete The Removal Of US Tariffs

-

New Premises8 hours ago

New Premises8 hours agoP. N. Gadgil & Sons Expands in Pune with New Store at Tribeca Highstreet; Launches 9KT Collection

-

National News11 hours ago

National News11 hours agoPalmonas Raises $40 Million in Series B, Accelerates Omni-Channel Expansion

-

DiamondBuzz8 hours ago

DiamondBuzz8 hours agoBotswana Stepping Up Diplomatic Efforts To Complete The Removal Of US Tariffs

-

BrandBuzz7 hours ago

BrandBuzz7 hours agoTriptii Dimri Launches Hues By Tanishq; Collection Showcases The Vibrant Colours Of Natural Gemstones