International News

Namibia’s Finance Minister Calls for Economic Diversification as Diamond Sector Weakens

Minister Shafudah Foresees Modest Growth for 2025 Amid Diamond Revenue Decline and Urges Focus on Alternative Sectors

In her recent budget speech, Namibia’s Finance Minister, Ericah Shafudah, emphasized the urgent need for economic diversification as the country faces continued challenges in its diamond sector. She forecasted only 4.5% growth for 2025, a downward revision from the previously projected 5.4%. The diamond industry, which contributes about 10% of Namibia’s GDP, has been facing several headwinds, including weak global demand, particularly from key markets like China and the US, increased competition from Angola’s cheap rough supply, and the growing popularity of lab-grown diamonds.

The slump in the diamond sector has had a significant impact on domestic activities, with total revenue from diamonds halving in 2024. Debmarine Namibia, the joint venture between De Beers and the Namibian government, reported a 38% decline in its revenue last year. This decline has been reflected in the country’s tax revenues, with Namibia’s Revenue Agency (NamRA) forecasting a reduction of NAD 6 billion (approximately USD 330 million) for 2025.

Minister Shafudah’s speech highlighted the urgent need for diversification, with Namibia possessing exceptional solar energy potential, along with opportunities for growth in tourism, agriculture, and manufacturing. By focusing on these sectors, Namibia aims to reduce its reliance on diamonds and build a more resilient economy capable of withstanding fluctuations in global commodity markets.

International News

Jewellery Was The Top Category For Global Luxury Spending In 2025: Bain & Company-Altagamma

Fundamental Shift in luxury consumption—from ownership to meaningful experiences, AI-driven shopping journeys

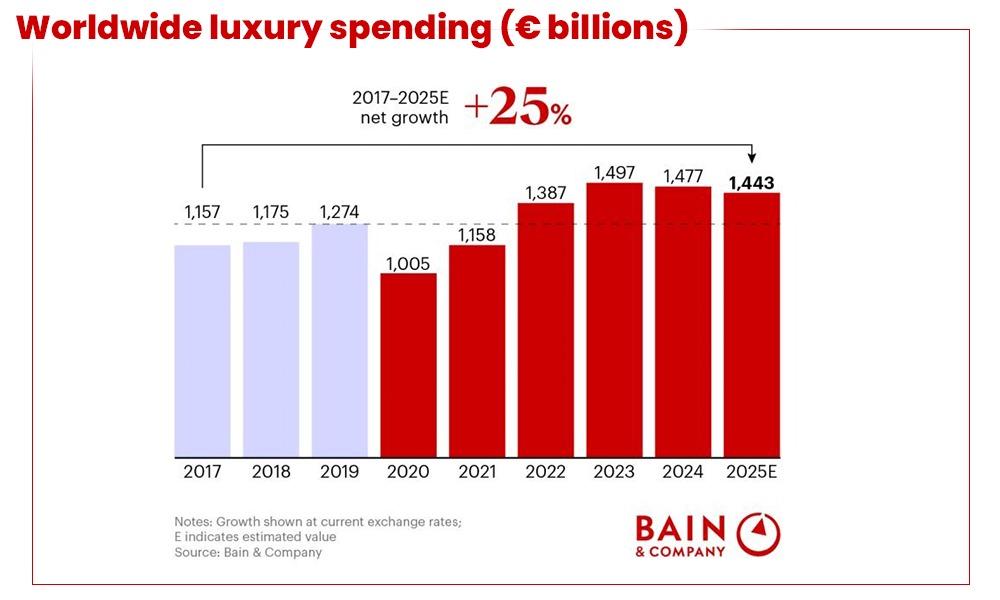

Despite economic uncertainty, geopolitical tensions, and changing consumer behaviour, the global luxury industry is showing signs of stabilization. According to the Bain & Company–Altagamma Luxury Goods Worldwide Market Study 2026, global luxury spending reached €1.443 trillion in 2025, with the personal luxury goods market expected to return to moderate growth in 2026. Jewellery was the top category for global luxury spending in 2025

The report highlights a fundamental shift in luxury consumption—from ownership to meaningful experiences, AI-driven shopping journeys, and greater demand for personalization. Brands that succeed will be those that strengthen cultural relevance, embrace AI, and deliver emotionally engaging experiences.

Key Highlights

- Global luxury spending reached €1.443 trillion in 2025 and is projected to grow 0–2% in 2026.

- The personal luxury goods market stood at €358 billion in 2025 and is expected to grow 2–4% in 2026, reaching €365–373 billion.

- Luxury experiences continue to outperform tangible goods, reflecting consumers’ preference for memorable experiences over ownership.

- Jewellery is the strongest-performing luxury category, followed by apparel, eyewear, and fragrances.

- Leather goods, footwear, and cosmetics remain under pressure, though recovery is gradually emerging.

- The Americas, led by the US, are driving growth, fuelled by younger consumers and expanding upper middle-class spending.

- Europe and the Middle East continue to weigh on market performance due to weaker tourism and geopolitical uncertainty.

- China is showing cautious recovery, with online luxury sales rising 25–35%, driven more by fashion than status-led purchases.

- Around 60% of luxury brands are now outperforming last year’s results, indicating improving market resilience.

- Nearly 50% of luxury shoppers consult the second-hand market before purchasing new products, underlining the growing importance of resale.

- Artificial Intelligence is transforming luxury retail, with half of consumers already using AI during their purchase journey for discovery and product comparison.

- More than 80% of the luxury market’s value is represented by brands that actively invest in sports sponsorships to build cultural relevance.

- Immersive luxury experiences—including bespoke travel, fine dining, and local cultural experiences—continue to gain popularity.

- Consumers increasingly associate luxury with personal fulfilment and meaningful living, rather than status or social recognition.

- Bain identifies three priorities for luxury brands:

- Deliver immersive, experience-led luxury.

- Build stronger cultural relevance across diverse consumer groups.

- Leverage AI for personalization and co-creation with customers.

The luxury industry is entering a new phase where growth will be driven less by products and more by experiences, emotional connections, AI-enabled personalization, and authentic brand meaning. While macroeconomic and geopolitical challenges remain, brands that adapt to evolving consumer expectations are well positioned for sustained growth.

Jewellery Was The Top Category For Global Luxury Spending In 2025: Bain & Company-Altagamma

Senco Gold & Diamonds Celebrates The Season Of Everyday Indulgence With ‘Drops Of Joy’

Gold and Silver Slip As Middle East Tensions Flare Again- AUGMONT BULLION REPORT

GJEPC Gears Up Industry For India–UK CETA Rollout; London Buyer-Seller Meet Opens New Trade Opportunities

Gold and Silver Slip As Middle East Tensions Flare Again- AUGMONT BULLION REPORT

Senco Gold & Diamonds Celebrates The Season Of Everyday Indulgence With ‘Drops Of Joy’

-

International News10 hours ago

International News10 hours agoGJEPC Gears Up Industry For India–UK CETA Rollout; London Buyer-Seller Meet Opens New Trade Opportunities

-

International News10 hours ago

International News10 hours agoGold and Silver Slip As Middle East Tensions Flare Again- AUGMONT BULLION REPORT

-

National News10 hours ago

National News10 hours agoSenco Gold & Diamonds Celebrates The Season Of Everyday Indulgence With ‘Drops Of Joy’

-

International News8 hours ago

International News8 hours agoJewellery Was The Top Category For Global Luxury Spending In 2025: Bain & Company-Altagamma