National News

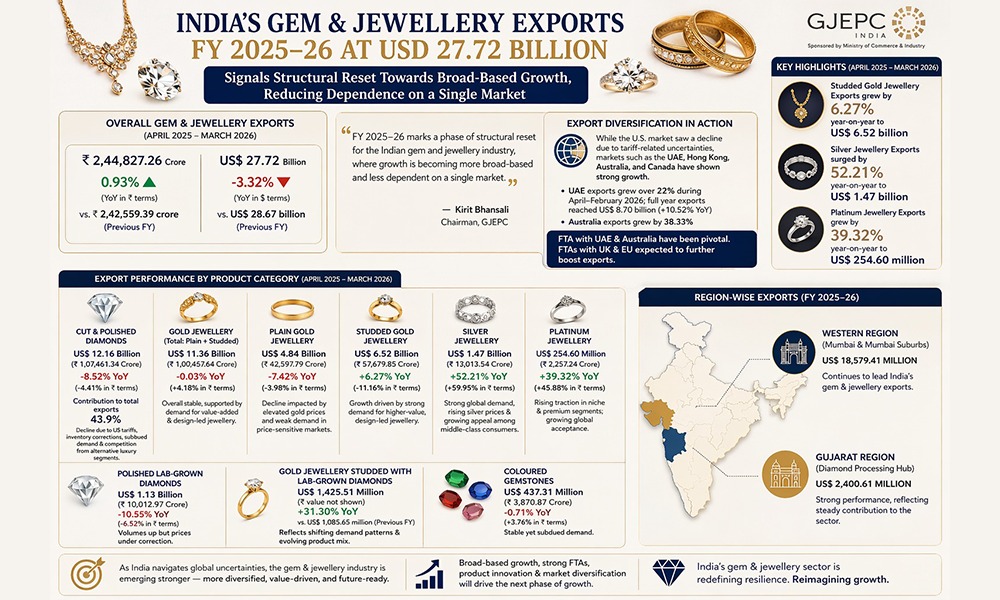

India’s Gem & Jewellery Exports in FY 2025–26 at USD 27.72 Billion Signal A Structural Reset Towards Broad-Based Growth, Reducing Dependence On A Single Market

For the FY 2025-26, Studded Gold Jewellery Exports Grew By 6.27% Year-On-year To US$ 6.52 Billion

- Silver jewellery exports surged significantly by 52.21% year-on-year to US$ 1.47 billion

- Platinum jewellery exports grew by 39.32% year-on-year to US$ 254.60 million

India’s gem and jewellery exports for the financial year April 2025 – March 2026 stood at Rs. 2,44,827.26 crore, registering a growth of 0.93% in rupee terms compared to Rs. 2,42,559.39 crore in the previous financial year. In dollar terms, exports were recorded at US$ 27.72 billion, reflecting a moderate decline of 3.32% year-on-year.

The performance comes amid a year marked by geopolitical uncertainties, evolving U.S. tariff regimes, and emerging tensions in West Asia, yet underscores a deeper transformation underway in India’s gem and jewellery export landscape.

Kirit Bhansali, Chairman, GJEPC, Said:

“FY 2025–26 marks a phase of structural reset for the Indian gem and jewellery industry, where growth is becoming more broad-based and less dependent on a single market. Exporters have actively diversified into new geographies, strengthened value-added segments, and adapted swiftly to evolving global trade dynamics.”

“Even as the U.S. market saw a decline due to tariff-related uncertainties, markets such as the UAE, Hong Kong, Australia, and Canada have demonstrated strong growth.”

“Free Trade Agreements with the UAE and Australia have played a pivotal role in supporting export diversification and sustaining growth momentum. While exports to the UAE witnessed strong growth of over 22% during April–February 2026, the emerging tensions in the region moderated the overall growth to 10.52% for the full financial year, with exports reaching USD 8.70 billion.”

“At the same time, markets like Australia have shown robust growth of 38.33%, reinforcing the importance of FTA-led market expansion in building a more resilient and broad-based export ecosystem. The anticipated implementation of FTAs with the UK and EU this year is expected to further support the growth of India’s gem and jewellery exports.”

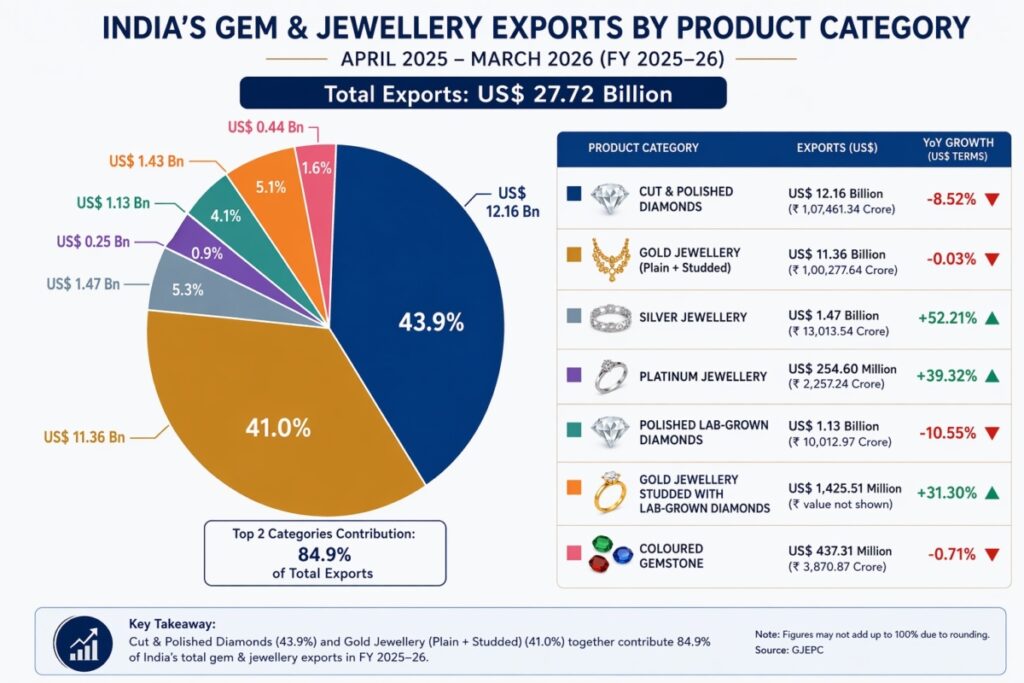

During April 2025–March 2026:

- Cut and polished diamonds remained the largest product category within the overall gem and jewellery basket, contributing 43.9% of total exports in FY 2025–26. Exports of cut and polished diamonds were recorded at US$ 12.16 billion (Rs. 1,07,461.34 crores), registering a year-on-year decline of 8.52% (-4.41% in rupee terms). This contraction was primarily influenced by the impact of US tariff increases implemented in the previous year, along with global inventory corrections, structural headwinds in key markets, subdued discretionary spending, and increasing competition from alternative luxury segments.

- Gold jewellery exports, including both plain and studded segments, remained largely stable at US$ 11.36 billion (Rs. 1,00,277.64 crores) in FY 2025–26, registering a marginal decline of 0.03% year-on-year (+4.18% in rupee terms).

- Within this, plain gold jewellery exports declined by 7.42% year-on-year (-3.98% in rupee terms) to US$ 4.84 billion (Rs. 42,597.79 crores), largely impacted by elevated gold prices, which weighed on demand, particularly in price-sensitive markets.

- On the other hand, studded gold jewellery exports grew by 6.27% year-on-year (+11.16% in rupee terms) to US$ 6.52 billion (Rs. 57,679.85 crores), supported by sustained demand for value-added, design-led jewellery. This growth reflects a clear shift in consumer preference towards higher-value products and underscores the resilience of the studded segment despite rising gold prices.

- Silver jewellery exports surged significantly by 52.21% year-on-year (+59.95% in Rs. terms) to US$ 1.47 billion (Rs. 13,013.54 crores). This outstanding performance was driven by strong global demand, supported by rising silver prices and increasing affordability appeal. Silver continues to gain traction among a growing middle-class consumer base, particularly in emerging markets, positioning it as a high-growth category with significant upside potential within the gem and jewellery sector.

- Platinum jewellery exports grew by 39.32% year-on-year (+45.88% in Rs. terms) to US$ 254.60 million (Rs. 2,257.24 crores), reflecting increasing traction in niche and premium segments. Exceptional growth reflecting increased global acceptance of platinum jewellery, representing a strategic opportunity.

- Polished lab-grown diamond exports declined by 10.55% year-on-year (-6.52% in rupee terms) to US$ 1.13 billion (Rs. 10,012.97 crores) in FY 2025–26, even as volumes increased, indicating ongoing price correction.

- At the same time, gold jewellery studded with lab-grown diamonds recorded a strong growth of 31.30%, rising to US$ 1,425.51 million from US$ 1,085.65 million in the previous year, reflecting evolving product segmentation and shifting demand patterns across jewellery categories.

- Coloured gemstone exports were recorded at US$ 437.31 million (Rs. 3,870.87 crores), witnessing a marginal decline of 0.71% year-on-year (+3.76% in Rs. terms), reflecting stable yet subdued demand.

Region-wise, exports from key gem and jewellery clusters across India showed varied performance. The Western Region, comprising major hubs such as Mumbai and Mumbai suburbs, continued to lead with exports worth US$ 18,579.41 million in FY 2025–26. The Gujarat Region, a key centre for diamond processing and manufacturing, also recorded strong performance with exports of US$ 2,400.61 million, reflecting its steady contribution to the sector.

India’s Gem & Jewellery Exports

| Rank | Countries | 2024-25 | 2025-26 | % Growth |

| US$million | US$million | (y-o-y) | ||

| 1 | United Arab Emirates | 7,868.16 | 8,696.27 | 10.52 |

| 2 | Hongkong | 4,559.14 | 5,972.24 | 30.99 |

| 3 | United States Of America | 9,236.46 | 5,087.33 | -44.92 |

| 4 | Belgium | 1,190.00 | 1,390.98 | 16.89 |

| 5 | United Kingdom | 777.69 | 711.72 | -8.48 |

| 6 | Thailand | 525.56 | 675.20 | 28.47 |

| 7 | Israel | 548.27 | 596.68 | 8.83 |

| 8 | Singapore | 529.39 | 566.02 | 6.92 |

| 9 | Australia | 260.41 | 360.21 | 38.33 |

| 10 | France | 266.60 | 356.12 | 33.58 |

| 11 | Canada | 148.63 | 319.57 | 115.01 |

| 12 | Others | 2,759.23 | 2,985.07 | 8.18 |

| Total | 28669.53 | 27717.40 | -3.32 | |

National News

Cosmos Diamonds Makes History With World’s First LGD Jewellery Launched Into Space

The Launch Also Reinforces India’s Emergence As A Global Innovation Hub Where Startups From Diverse Sectors Are Forging Unconventional Partnerships.

In a landmark moment where luxury, science and space exploration converged, Sanjana Tripuramallu, founder of Bengaluru-based Cosmos Diamonds, has achieved a global first by collaborating with private space company Skyroot Aerospace to send Cosmos Bloom, the world’s first lab-grown diamond (LGD) jewellery creation into space aboard the Vikram-1 rocket.

The Cosmos Bloom Diamond is handcrafted in 18 kt gold using 32 pear-cut LGDs arranged in the form of a blooming lotus and mounted on a specially engineered aluminium base plate. It is designed to withstand the extreme conditions of launch and spaceflight. The space-bound jewel is valued at Rs 11 lakh and combines Indian craftsmanship, technology, and innovation.

Sanjana Tripuramallu, Founder- Cosmos Diamonds

The launch also reinforces India’s emergence as a global innovation hub where startups from diverse sectors are forging unconventional partnerships. While Skyroot Aerospace showcased the country’s private launch capabilities through Vikram-1, Cosmos Diamonds used the mission to tell a powerful story of Indian design and scientific ambition on an international stage. With the successful launch of the world’s first lab-grown diamond jewel into orbit, Sanjana Tripuramallu and Cosmos Diamonds have etched their names into both jewellery and space history, demonstrating that the future of luxury may well extend beyond Earth itself.

Precious Metals Bounce Back As Iran Ceasefire Hopes Rise, But Fed Rate Fears Loom: AUGMONT BULLION REPORT

Bvlgari Revives Its Iconic Gold & Steel Legacy With Bold New Jewellery Creations

Cosmos Diamonds Makes History With World’s First LGD Jewellery Launched Into Space

Precious Metals Bounce Back As Iran Ceasefire Hopes Rise, But Fed Rate Fears Loom: AUGMONT BULLION REPORT

MCX Gold, Silver Futures For August Delivery Rise On Renewed Geopolitical Tensions

Cosmos Diamonds Makes History With World’s First LGD Jewellery Launched Into Space

-

National News5 hours ago

National News5 hours agoMCX Gold, Silver Futures For August Delivery Rise On Renewed Geopolitical Tensions

-

International News46 minutes ago

International News46 minutes agoPrecious Metals Bounce Back As Iran Ceasefire Hopes Rise, But Fed Rate Fears Loom: AUGMONT BULLION REPORT

-

National News2 hours ago

National News2 hours agoCosmos Diamonds Makes History With World’s First LGD Jewellery Launched Into Space

-

International News5 hours ago

International News5 hours agoLondon Diamond Bourse Announces Launch Of Its New Coloured Gemstone Course